Quo vadis, aurum?

“Tomorrow belongs to those who can hear it coming.”

David Bowie

Key Takeaways

- A profound change is taking place before all our eyes, a monetary climate change. What was today the immutable framework within which we operated seems tomorrow to be no more than a relic of the past.

- This monetary climate change has far-reaching implications – for monetary policy, fiscal policy and investment decisions.

- Traditional, mixed portfolios are subject to significantly higher risk in an inflationary environment, as correlations can break down and both asset classes can suffer significant losses. This is because negative correlation between stocks and bonds is the exception rather than the rule. In 70 of the last 100 years, stocks and bonds have been positively correlated.

- This year, we would also like to venture an outlook on the future price of gold. The implied distribution density function of the gold options market shows that with a probability of almost 45% we will see a new 52-week high – USD 2,100 or higher – in December 2021 and thus also a new all-time high in the gold price at the same time.

When Richard Nixon announced the “temporary” suspension of the convertibility of the US dollar into gold on August 15, 1971,[1] no one knew that the closure would last 50 years. It turned out that it was not a temporary measure but a permanent stopgap. Today, half a century later, there is nothing to suggest that this suspension will be voluntarily ended in the foreseeable future. Global fiat money is the convention of today. Gold backing is even forbidden in the Articles of Agreement subscribed to by all members of the International Monetary Fund.[2]

From our point of view, the dematerialization of the monetary system sealed its unsustainability and its limited lifespan. Nevertheless, courageous central bankers such as Paul Volcker, Karl Otto Pöhl, and Fritz Leutwiler were able to ensure that the money-creation privilege was not unduly strained even in the era of an uncovered money system. If one listens closely, however, doubts prevailed even in central bank circles as to whether the system could be continued indefinitely in this form. Alan Greenspan made the following comments in 2002:

“In the past there has been considerable evidence that fiat currencies in general have been mismanaged and that inflation has too often been the result. (…) We are learning how to manage a fiat currency. I have always had some considerable skepticism about whether that in the long run can succeed, but I must say to you the evidence of recent decades is that it has been succeeding. Whether that continues is a forecast which I can’t really project on.” [3]

The Monetary Consequences of the Covid-19 Pandemic

Today, shortly before the 50th anniversary of this drastic monetary change, only a few economists recognize a new fundamental change – possibly because this time the change has been more gradual. It is a process whose start cannot be pinpointed to an exact date. However, it is clear to critical observers that the fiscal and monetary policy interventions during the coronavirus crisis have taken us into a new dimension and will have profound, irreversible consequences that will only fully unfold over a period of years. However, the prevailing narrative regarding the global monetary weather situation continues to be that we are only experiencing some transitory cloudiness in the form of temporarily higher inflation rates.

We are of a completely different opinion. A profound change is taking place before all our eyes, a monetary climate change. What today seems still to be an irrevocable framework within which we move, will prove tomorrow to be no more than a broken-down relic. The Covid crisis has the potential to shake up the unbacked monetary system and could ultimately shorten its remaining life expectancy significantly.

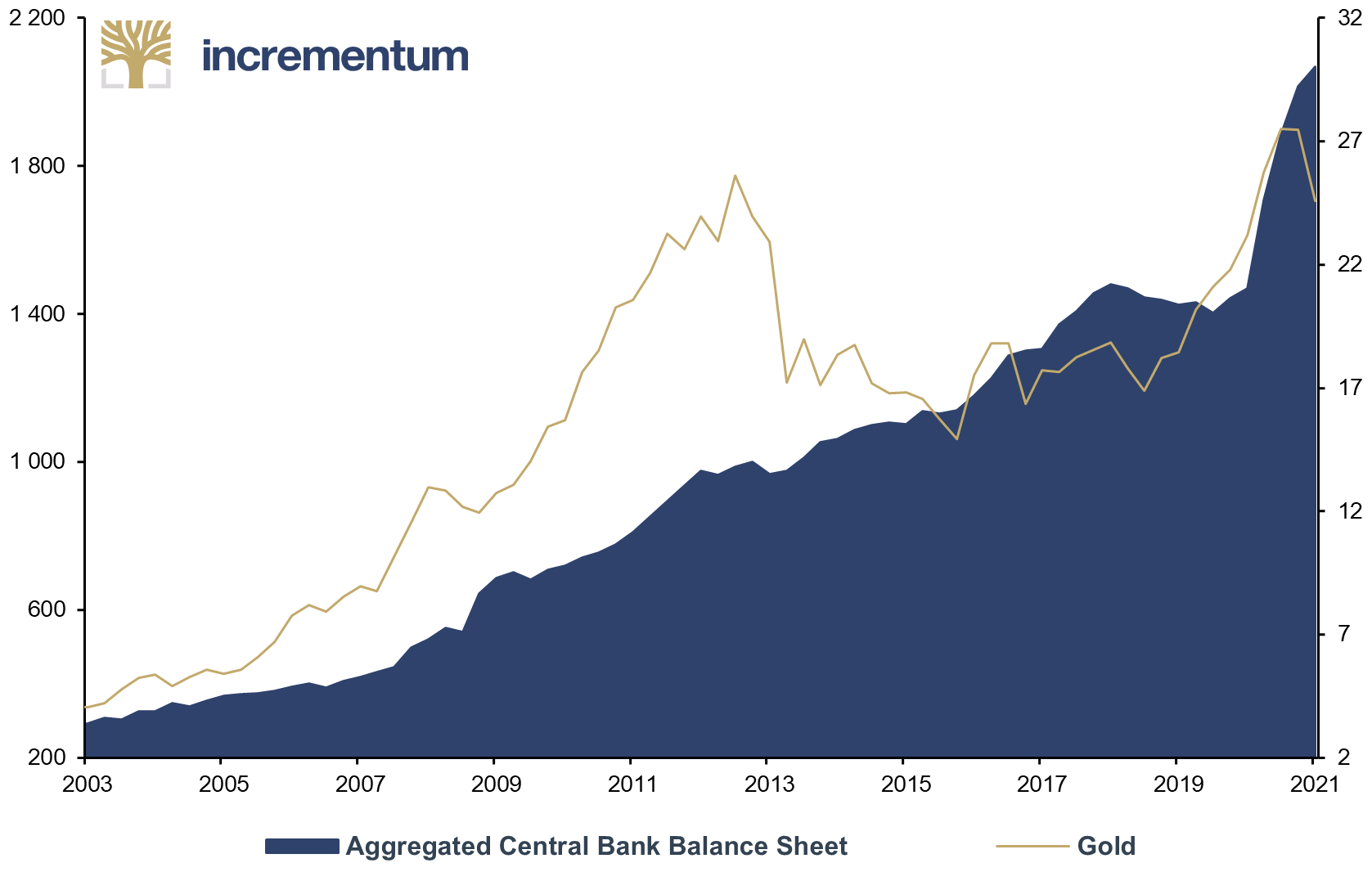

Gold (lhs), in USD, and Aggregated Central Bank Balance Sheet of SNB, FED, PBoC, BoJ, and ECB (rhs), in USD trn, Q1/2003-Q1/2021

Source: Murenbeeld, Reuters Eikon, Incrementum AG

At the heart of this change is the new economic zeitgeist of fiscal and monetary policymakers. Thus, it is increasingly claimed that overindebtedness has no serious consequences. It is assumed that the digital printing press can be operated at will to monetize debt. It is postulated that monetary inflation has no impact on price inflation. And it is even declared to be the goal to create higher inflation rates rather than guard the purchasing power of the currency.

Redefinition of Price Stability

Let us look at the primary monetary policy objective of the ECB – and of many other central banks – “price stability”. By price stability, the ECB means a price increase in the basket of goods “of close to, but below, 2% over the medium term”. This is a rather peculiar interpretation of “stability”, because if consumer prices rise by 2% a year, this corresponds to a loss of purchasing power of just under 22% in 10 years and more than 48% after 20 years.

As part of the ECB’s strategy review currently underway, this target definition is being subjected to a comprehensive analysis.[4] As the official inflation rate has been too low in recent years, numerous ECB representatives are advocating higher inflation rates in the future to “compensate” for the supposedly insufficient rise in consumer prices.[5] In doing so, the ECB would be following in the footsteps of the Federal Reserve.

In fact, the main argument for the previous price stability target of inflation “close to, but below 2%” was that there should always be a buffer to the 0% mark. At no time should falling consumer prices be permitted, because in the eyes of the ECB’s Governing Council – and almost all economists – the dreaded deflationary spiral would set in. Despite official inflation rates that are “too low” in some areas, the drift into a deflationary spiral has not occurred in recent years. The same narrative applies to the US dollar, which is therefore steadily losing purchasing power and will continue to do so. And even a small increase in the inflation rate in absolute terms would significantly accelerate the loss of purchasing power over the next 10 years.

US Dollar Purchasing Power Loss and Projections, 2001-2031

Source: Reuters Eikon, Incrementum AG

Courtesy of Hedgeye

Now that inflation rates have already risen significantly again, according to this line of reasoning it does not make the slightest sense to orchestrate or allow even higher inflation. In our opinion, the new chain of reasoning for a symmetric inflation target is not stringent. It is obvious that higher inflation rates represent a thoroughly intentional demonetization to relieve countries that are heavily indebted. However, two aspects must be considered.

On the one hand, a surge in inflation implies a transfer of wealth from creditors to debtors. On the other hand, an inflationary dynamic that sets in is difficult to get under control again. It is not for nothing that central bankers have coined the phrase “Don’t let the inflation genie out of the bottle”.

Inflation as a Risk for Stock and Bond Markets?

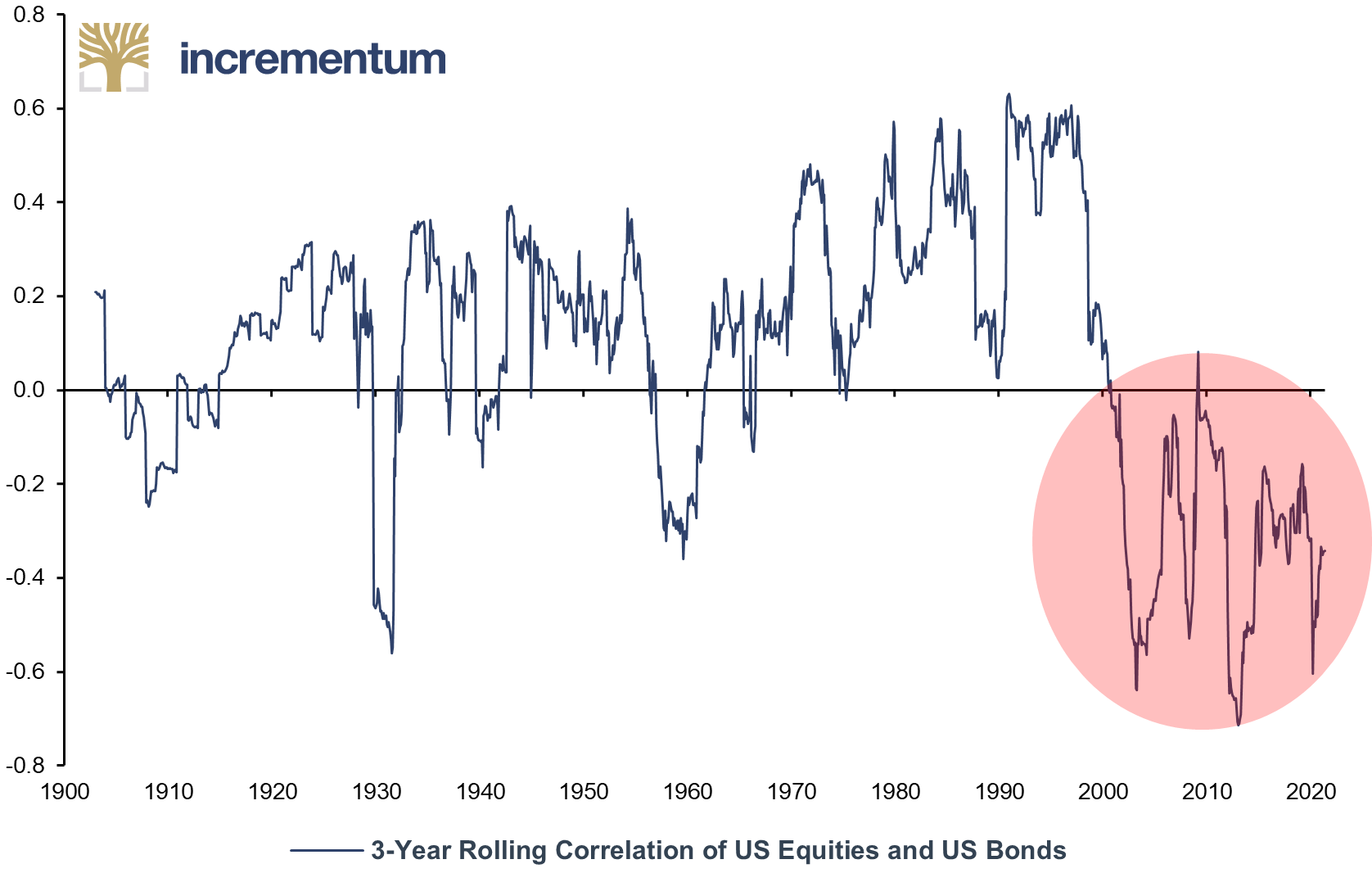

Four decades of disinflation and falling interest rates have left their mark on the financial markets in particular. Both the stock and bond markets had a structural tailwind from falling inflation rates. The valuation of both asset classes benefited, as future cash flows were discounted at an ever-lower interest rate, driving up valuations. The classic 60/40 portfolio, consisting of 60% equities and 40% bonds, was able to generate respectable returns with moderate risk during this period, as the asset classes complemented each other well.

As we have already shown in our In Gold We Trust report 2019,[6] traditional mixed portfolios are subject to significantly higher risk in an inflationary environment, as correlations can break down and both asset classes can suffer significant losses. This is because negative correlation between stocks and bonds is the exception rather than the rule. In 70 of the last 100 years, stocks and bonds have been positively correlated.

3-Year Rolling Correlation of US Equities (S&P 500) and US Bonds (UST10Y), 01/1900-05/2021

Source: Reserve Bank of Australia, Nick Laird, goldchartsrus.com, Reuters Eikon, Incrementum AG

The longer we remain at zero or negative interest rates, the riskier bonds become, as they no longer have any appreciation potential, but they do have a significant – inflation-driven – interest rate risk and possibly also a default risk. It is no coincidence that low-yielding bonds have for some time been classified by many market participants as a “returnless risk”.

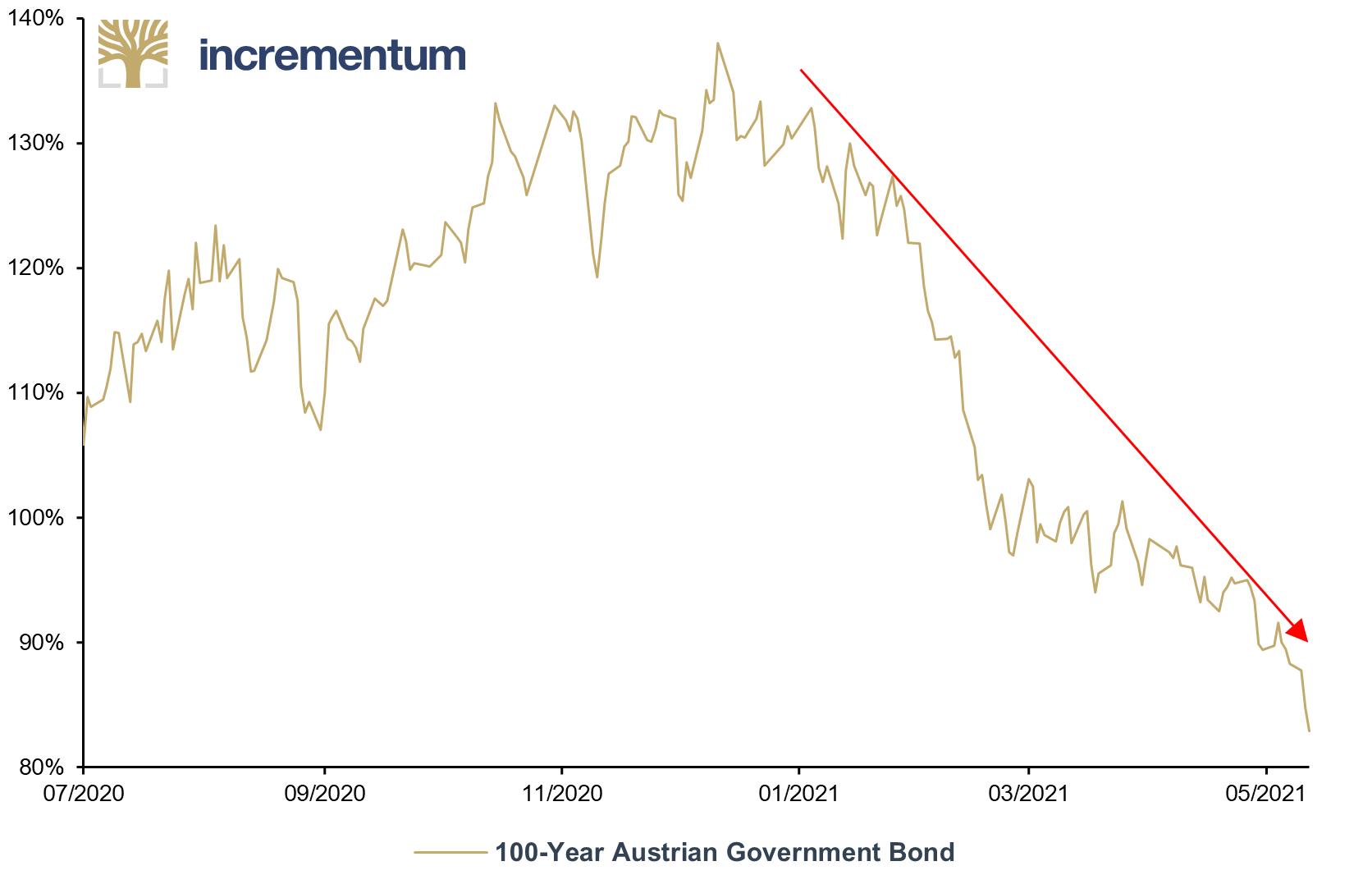

The longer the remaining term of the bond, the greater the impact of even small increases in bond yields on the market value of a bond. Even if inflation is moderately higher than expected, holders of long-dated paper will be deprived of a significant portion of their purchasing power. As the following chart of the Austrian century bond shows, even a small increase in yield from 0.45% to 1.13% triggers a price loss of more than 36% since the beginning of the year. Whether many investors are aware of this, especially those who hold bonds indirectly, e.g. in pension or life insurance policies, may be seriously doubted.

100-Year Austrian Treasury, June 30, 2120, 07/2020-05/2021

Source: Frankfurt Stock Exchange, Incrementum AG

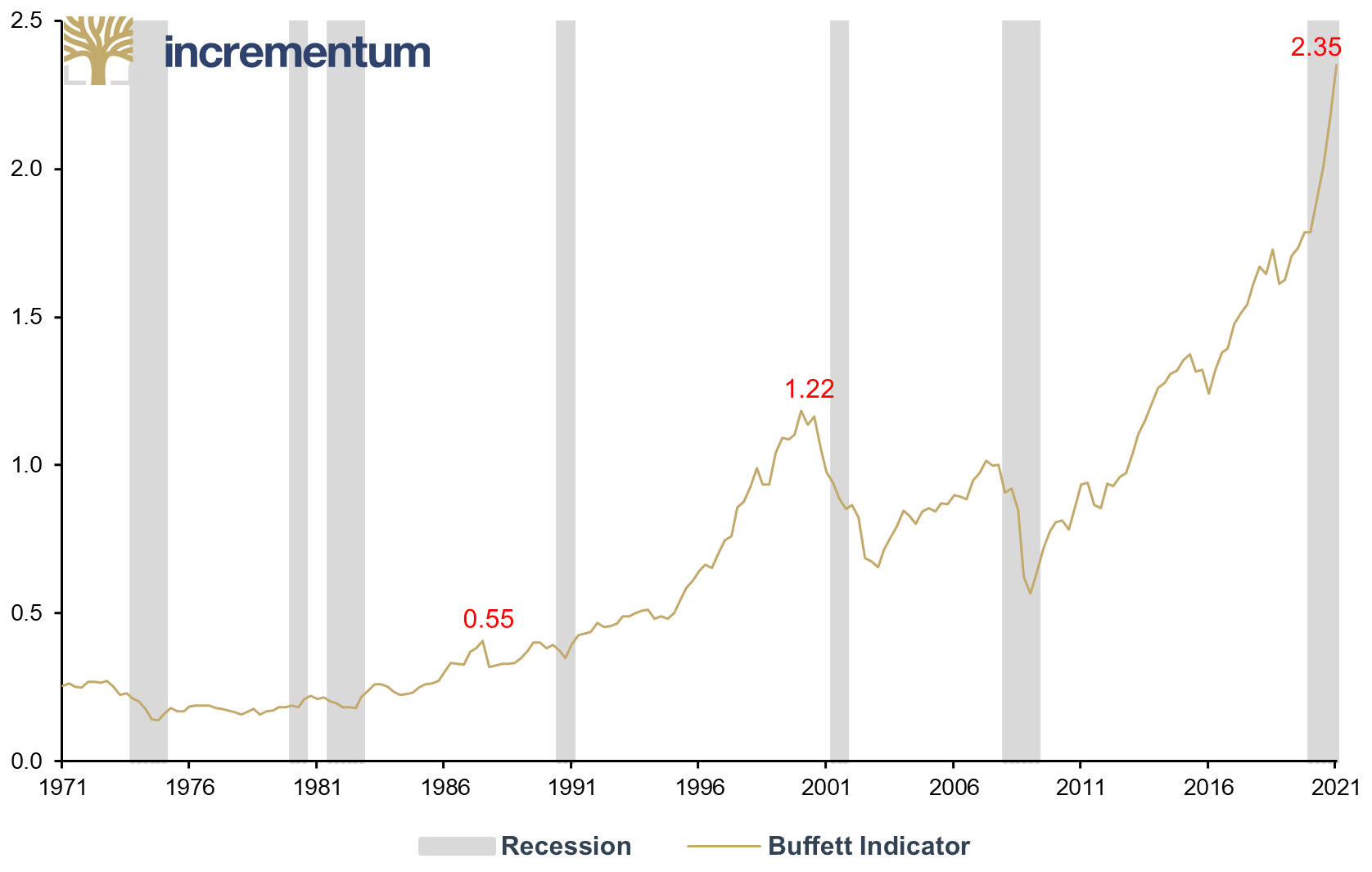

However, the miserable profitability of bonds has also had a significant impact on equities. It is not without reason that for years equities have been regarded as having no alternative. As a result, valuations on the stock markets have risen dramatically. The CAPE ratio is currently at a value of 37, twice as high as in 2011, when gold marked its last all-time high before August 2020. According to the Buffett indicator[7], the valuation of the stock market compared to US GDP is currently at record levels. It is astonishing that the Buffett indicator rose during a recession for the first time in history.

Buffett Indicator, Q1/1971-Q1/2021

Source: Federal Reserve St. Louis, Wellenreiter-Invest, Incrementum AG

Much of what is currently happening on the capital markets is reminiscent of the term crack-up boom, coined by Ludwig von Mises. It is amazing that the market capitalization of the stock markets is now more than USD 20trn higher than before the outbreak of the Covid-19 pandemic. We find it implausible that those higher valuations are justified.

Bloomberg World Exchange Market Capitalization, in USD trn, 01/2018-04/2021

Source: Bloomberg, Incrementum AG

History Rhymes

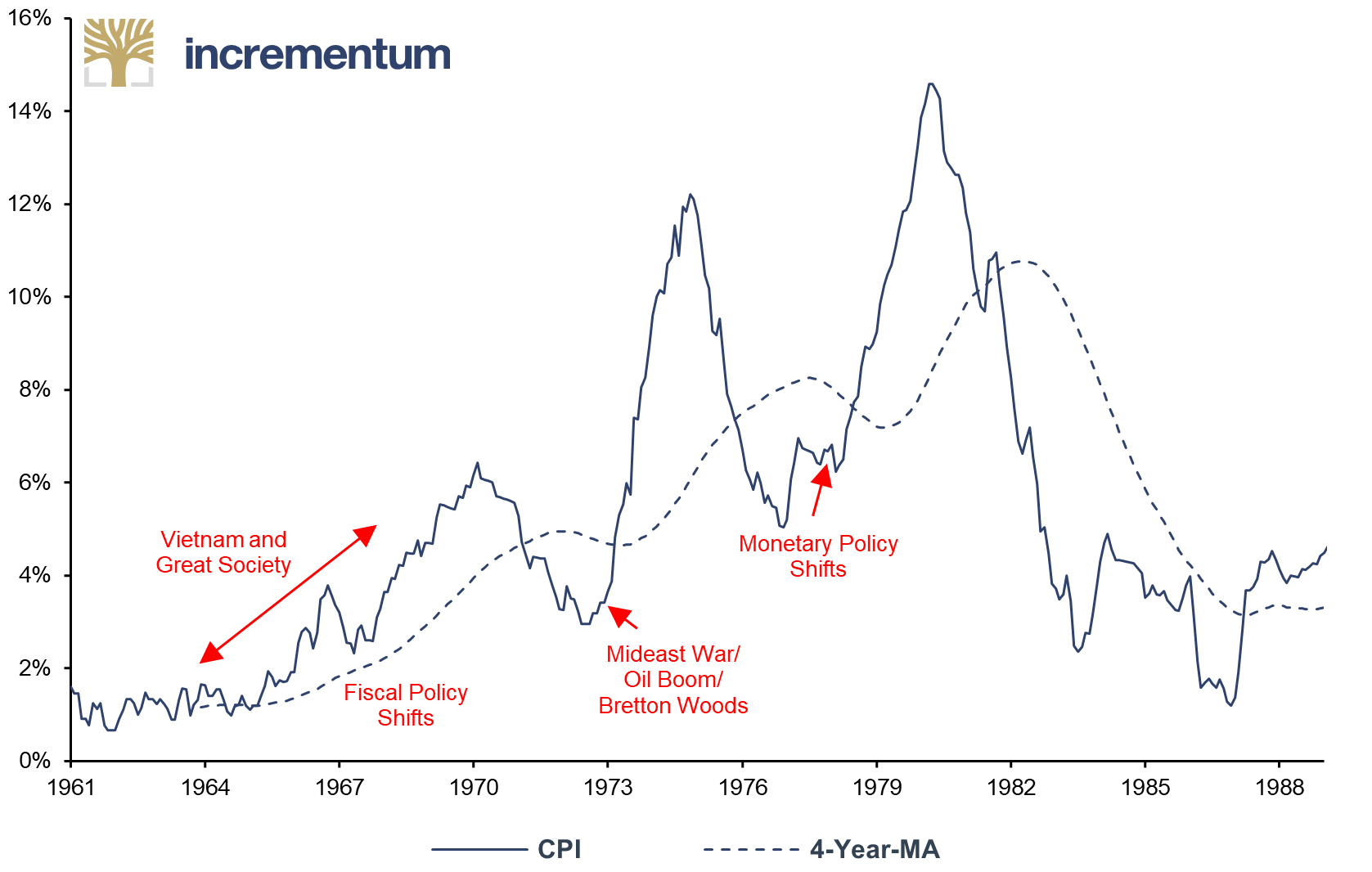

The consistently buoyant situation on the financial markets in recent years could experience a lasting change in the weather as a longer-term inflationary phase takes hold. To support this thesis, let us look to the past. We know that history does not exactly repeat itself, yet we find it interesting that the 2020s show similarities to the 1960s in some socioeconomic terms.

The period from 1963 to 1970 was marked in the USA by the so-called guns vs. butter[8] debate.[9] Guns referred to the financing of the Vietnam War, butter to President Lyndon B. Johnson’s costly Great Society programs. In the end, there was no backsliding on either military or social policy issues. Prestige projects such as the space race also continued to strain the national budget. Fiscal policy consequently became much more expansionary; instead of “guns or butter”, it was “guns and butter”.

There was also an attempt to structurally strengthen workers’ rights. The new policy favored unions over nonunionized workers. One result of all these measures was an increase in the CPI inflation index from 2% to 6% over a 7-year period.

There are also interesting parallels throughout among the actions of leaders. Just like President Biden, President Johnson was a former vice president. He believed that government intervention could improve people’s lives. We find similar approaches today in Biden’s American Families Plan and „American Jobs Plan. Unlike Biden, however, Johnson cut taxes. Still, the general thrust in the 1960s of a massive turnaround in government policy, to spend as much money as necessary to win the Vietnam War and to defeat poverty, can be seen equally in the second Covid-19 package of measures and income support for American families and workers, totaling over USD 4trn. Wages and salaries grew by about 32% during the 1960s, the fastest growth rate in the postwar era. President Biden is also placing a strong focus on increasing wages. This could have additional inflationary consequences over the years if a wage-price spiral develops.

Wages and Salary Accruals, in % of GDP, Q1/1951-Q1/2021

Source: Federal Reserve St. Louis, Incrementum AG

Socially, the defining feature of the 1960s may have been the polarization of the nation. Currently, the US seems to be even more divided than it was back then. The increased potential for conflict became clear during Donald Trump’s term in office. The division runs right across diverse social groups: conservatives versus progressives, the poor versus the rich, whites versus blacks, the Boomer generation versus Generation X, etc.

In the 1960s, the geopolitical focus was on a trial of strength with the supposedly rising Soviet Union. The consequence was a costly arms race and an expensive space race. The US may now be headed for a similar period of a new cold war, but this time with China as a rival, increasingly challenging the tottering hegemon.

All these developments – along with monetary policy changes – were the foundation for the inflationary decade of the 1970s.

The Great Return of Inflation

The likelihood of a sustained period of inflation will increase to the extent that the wage-price spiral begins to turn. Wage negotiations in the coming months and the rhetoric accompanying them will provide valuable information on how far monetary climate change has already progressed. It will also become clear how much governments are willing to adjust social benefits and pension payments in line with rising inflation, increases that in turn will make budget consolidation more difficult. This pattern was a major transmission element of price increases in the 1970s.

CPI, yoy%, 01/1961-01/1989

Source: Bloomberg, Reuters Eikon, Incrementum AG

Photo credit: commons.wikipedia.org

IIN instead of WIN?

We are still a long way from the overheated inflation climate of the 1970s. Price increases became a dominant sociopolitical issue as early as the mid-1970s. What MAGA – “Make America Great Again” – was for Donald Trump, the slogan WIN – “Whip Inflation Now” was for then US President Gerald Ford in response to the first wave of high inflation in 1974/75.[10] Currently, we see exactly the opposite development: It seems as if IIN – “Increase Inflation Now” – is the credo of today’s central bankers, economists and politicians.

We have been registering this fundamental change for some time now. That is why we decided last fall to publish an In Gold We Trust special entitled “The Boy Who Cried Wolf”.[11] In it, we point out how underestimated the risks of a significant pickup in inflation generally are. Many market participants are still unaware of how unpleasant the inflationary 1970s were, for equity investors as well as bond investors. It is therefore high time to take a close look at the risk to one’s portfolio posed by inflation and financial repression.

A key indication that the financial world is ill-prepared for monetary climate change is the fact that there are almost no fund managers on duty today who have experienced an inflationary environment during their active investment careers. The bulk of investment managers could be caught on the wrong foot. In addition, most portfolio strategies are based on back calculations that go back 10, 20, or at most 30 years. However, very few portfolio strategies still consider the inflationary environment of the 1970s.

Monetary System in Burnout

Investors must always think in terms of impact chains and take opportunity costs into account. In his superb book Antifragile: Things That Gain from Disorder, Nassim Taleb describes how important the frequency of stressors, i.e. stress-causing internal and external stimuli, is. This is because people cope better with acute stress than with chronic continuous stress. This is especially true when acute stress is followed by a long phase of recovery. To understand how damaging even a low-threshold stress factor with a protracted recovery can be, just consider the so-called Chinese water torture: Drops of water are continuously dropped on the head of the victim, who is to be made docile by the continuous stress.

In our opinion, the financial and monetary system is now in a state of permanent stress, just short of burnout. This is also reflected in the fact that for years now, only extraordinary measures have been applied in monetary policy, after ordinary monetary policy no longer worked. Therefore, theories such as MMT have now finally entered the mainstream.

Best of In Gold We Trust Report 2021

Other key findings from this year’s In Gold We Trust report, „Monetary Climate Change“, include the following:

- Portfolio characteristics of gold: Gold performs better when the yield curve is steepening than when it is flattening. This correlation reduces the likelihood that gold’s interim disappointing performance in recent months was due to the rise in nominal interest rates. Our research also shows that the correlation between gold and gold mining stocks increases significantly during periods of falling real interest rates. The increased sensitivity between these assets signals that the market views both as safe havens against inflation. Instead of betting only on gold, investors could use both as inflation hedges.

- De-dollarization: In the reshaping of the global monetary order, China continues to work on all fronts to undermine the hegemony of the US dollar. In this struggle, China has opened another front, the digital front. While the digital yuan is already making its first real-world test runs, the euro zone is only in the early planning stages, while the Federal Reserve does not appear to be taking action on the digital central bank currency (CBDC) front. China could use the 2022 Winter Olympics in Beijing to put on a show of CBDC performance. These developments aside, central banks once again emerged as net gold buyers in 2020, albeit at lower levels. It is noteworthy that Hungary recently tripled its gold reserves and Poland announced a significant increase in gold reserves in the coming years.

- ESG: Mining companies have embraced the general precepts of ESG and are integrating its values into their business models. ESG has thus become an integral part of the corporate DNA in the mining sector. Investors also benefit as they gain assurance that their investments do not conflict with ESG concerns. What remains challenging is the fact that there is no single framework and that the now-numerous rating agencies take very different, and thus difficult to compare, approaches to ESG.

- Mining stocks: In 2020, gold producers recorded their most profitable year in history. The average spot gold price rose to USD 1,770/oz., but average industry AISC remained flat. While the gold price set new all-time highs last year, the valuation of gold mining companies does not yet reflect the sharp increase in profitability. Currently, gold mining stocks have the highest margins and lowest valuations of any S&P 500 sector. The potential returns for the next few years may surprise even the most hardened gold bugs. We are likely still in the early stages of the bull market, as mining stocks remain undervalued despite their 2020 performance.

- Bitcoin & gold: In our In Gold We Trust report 2019, we explained the advantages of a combined investment strategy consisting of gold and Bitcoin and presented theoretical portfolio developments.[12] Since we are convinced of this strategy, we have launched an investable fund strategy, whose realized results to date we presented and analyzed in this report. The investment results so far confirm our thesis that gold and Bitcoin are stronger together in a noninflationary hard money portfolio.

- Silver: Monetary climate change should boost silver. Contrary to the widespread belief that everything will be the same after the Covid-19 pandemic, we are convinced that after 40 years of a disinflationary climate we are witnessing a fundamental shift towards an inflationary climate. Therefore, investment demand for silver will be the most important price driver in the current decade. The so-called green turn will also be beneficial for silver, as silver is an important industrial metal in many future green technologies.

- Technical analysis: The Coppock indicator generated a long-term buy signal at the end of 2015, and now it seems that the cup-handle formation will soon resolve to the upside. The price target of this formation is USD 2,700.

What Gold Price Does the Options Market Expect?

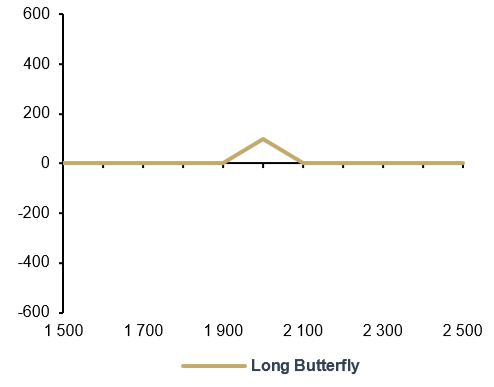

This year we would again like to venture an outlook on the future gold price. In contrast to last year’s 10-year price forecasts, which we calculated by means of our proprietary gold price model[13], this year we focus on a much shorter forecast period. The following model attempts to determine a probability distribution of hypothetical returns based on implied expectations in the gold options market, using long butterflies[14] , schematically outlined in the following two charts, as the basis for calculation.

Long Butterfly Line-Up, Gold Price at Expiration (x-axis), and Gross payoff (y-axis)

Long Butterfly, Gold Price at Expiration (x-axis), and Gross payoff (y-axis)

Source: Incrementum AG

This approach aims to calculate the fair price of the butterfly spread and repeat this process for all desired strike prices to generate a string of probabilities at different prices at the end. Due to the low liquidity of some gold December option contracts when using a 10-strike rhythm, we performed the calculation using a 50 strike rhythm.[15] Specifically, we use this to calculate the probabilities of certain scenarios occurring for the gold price in US dollars by the end of the year.[16] Consequently, we can derive the probability of the gold price reaching a new all-time high in December 2021.

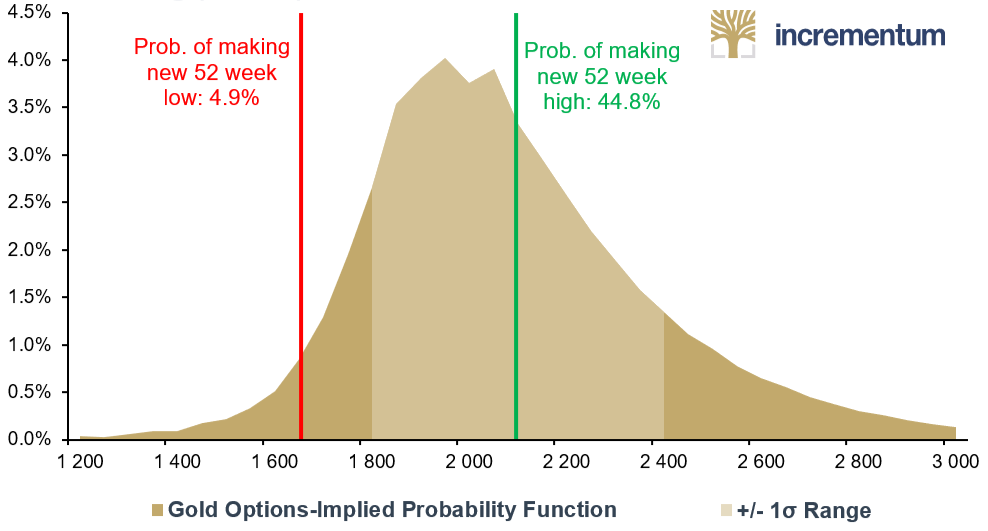

The following chart shows the implied distribution density function of the gold options market. This states that with a probability of almost 45% we will see a new 52-week high – USD 2,100 or higher – in December 2021 and thus also a new all-time high for the gold price at the same time. On the other hand, the probability that we will see a new 52-week low (USD 1,650 or lower) is less than 5%.[17]

Gold Options-Implied Probability Function, Exponential Smoothing (α = 0.2), December 2021

Source: Reuters Eikon, Incrementum AG

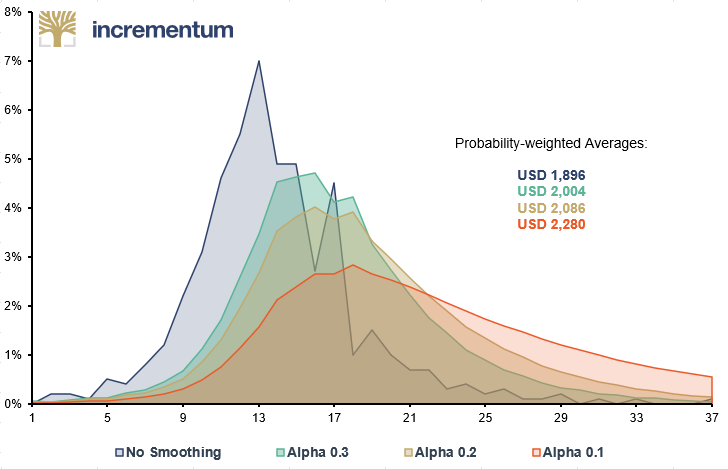

The next chart shows all the collected distribution density functions with their probability-weighted gold prices for December 2021, oscillating between USD 1,896 and USD 2,280.[18]

Gold Options-Implied Probability Distribution Functions, December 2021

Source: Reuters Eikon, Incrementum AG

The chart further shows that especially the strikes at USD 1,950 and USD 2,050 deviate from the overall distribution, likely because of the illiquidity of these options contracts. This reinforces the use of exponential smoothing of the distribution density function, which more realistically represents true market expectations.

Of course, this is only a snapshot. We are aware that expectations on the financial markets are generally not rigid. Nevertheless, the information content that can be derived from this analysis can be classified as quite high and roughly in line with our expectation for gold price development for the current calendar year.

Quo vadis, aurum?

Last year, our assessment was that a golden decade had begun for precious metals investors. In a conservative scenario, we had set a price target of USD 4,800 for the end of the decade. If the decade was plagued by stronger inflation, a price of USD 8,900 could be expected at the end of the decade. With the monetary climate change that we are witnessing this year, the risk of inflation is growing visibly.

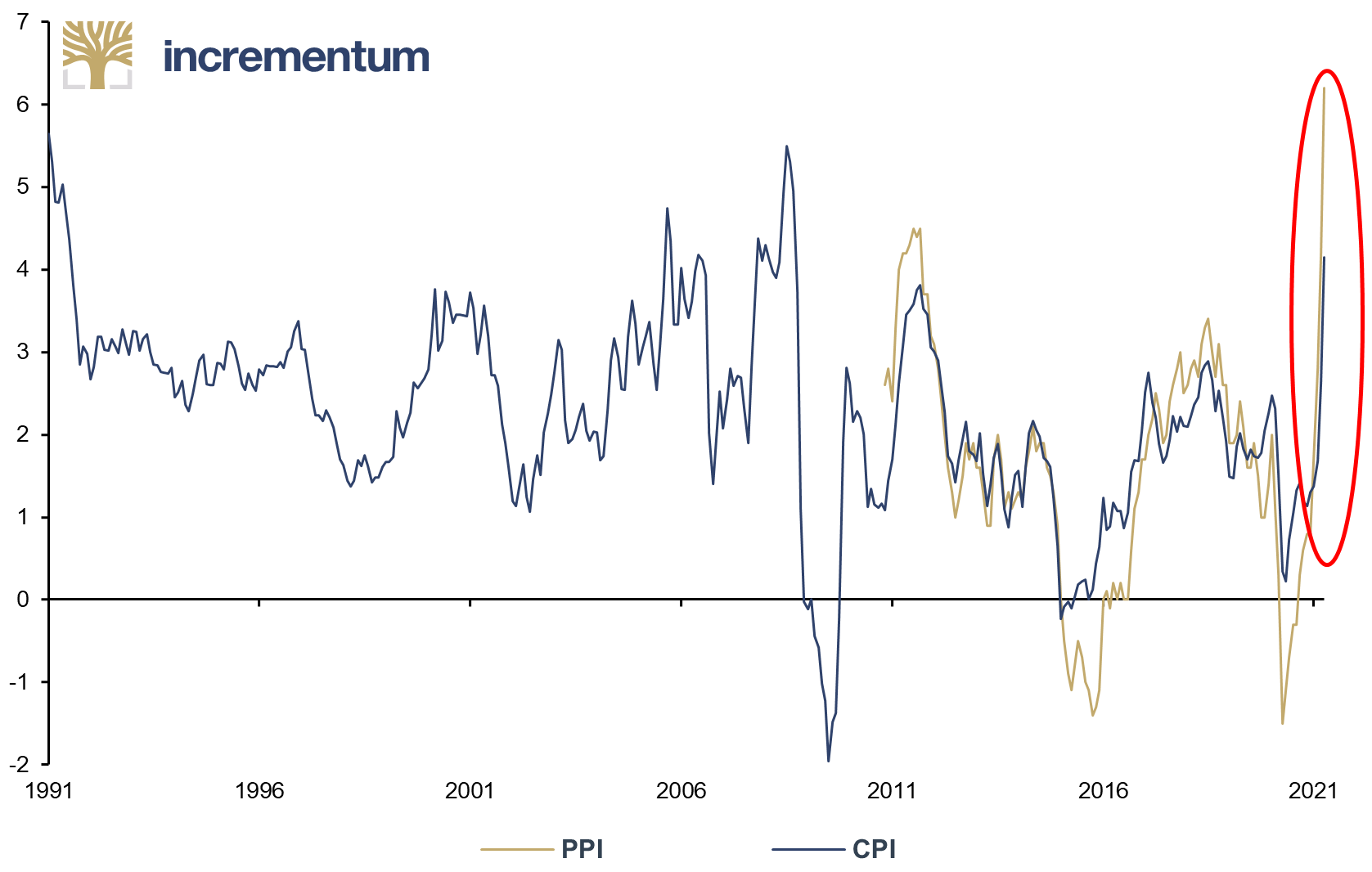

Admittedly, it is still too early in 2021 to say with any certainty how pronounced or how long the inflationary phase will affect everyday life. Nevertheless, we remain true to our 10-year forecast. From today’s perspective, the probability of a gold price at the upper end of the range has increased significantly. This has been impressively confirmed by the latest inflation figures in the US. Both consumer prices and producer prices have been significantly higher than expected this year.

CPI and PPI, yoy%, 01/1991-04/2021

Source: Reuters Eikon, Incrementum AG

Courtesy of Hedgeye

Many market participants do not yet recognize the monetary climate change. In recent months, markets have consistently reacted to higher-than-expected inflation figures with rising yields and falling gold prices in the short term. This reflects the expectation that inflation will be effectively fought by central banks and will remain a temporary phenomenon. As we have explained in detail, we disagree.

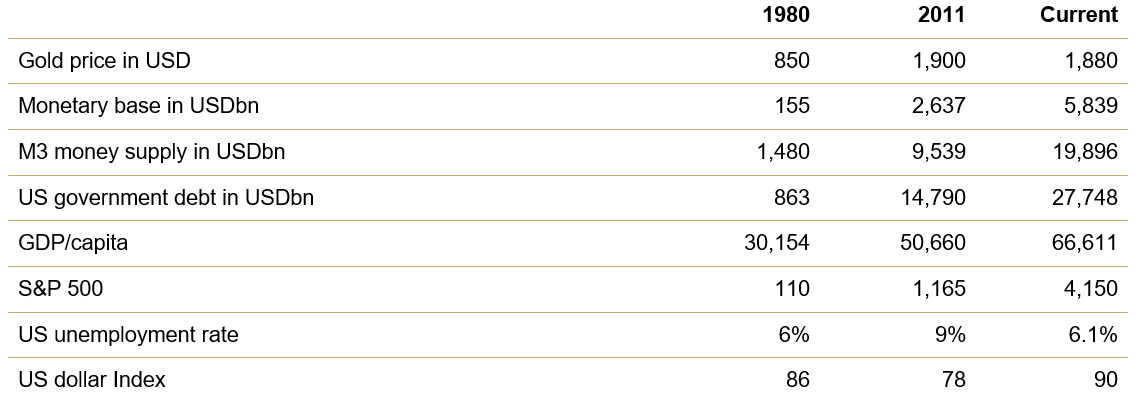

Conversely, it is therefore difficult to imagine that we are currently at the end of a gold bull market. When we compare various macro and market metrics at the time of the last secular all-time highs in 1980 and 2011 with the current situation, the gold price still appears cheap in relative terms.

Macro and market metrics at all-time highs of gold: 1980, 2011, current

Source: Federal Reserve St. Louis, Reuters Eikon, Incrementum AG, as of 05/20/2021

Despite an environment that should, by and large, be clearly supportive of gold, the gold price today is at about the same level as it was 10 years ago and is therefore, in our view, favorably valued. Ray Dalio, one of the most successful fund managers of all time, has recently commented several times on inflation and the merits of investing in gold. We would like to close with this thought of Ray Dalio, which also explains our motivation for publishing such a “tome”:

“I believe that the reason people typically miss the big moments of evolution coming at them in life is that we each experience only tiny pieces of what’s happening. We are like ants preoccupied with our jobs of carrying crumbs in our minuscule lifetimes instead of having a broader perspective of the big-picture patterns and cycles, the important interrelated things driving them, and where we are within the cycles and what’s likely to transpire.” [19]

The stability of the value of money is always a measure of confidence in the economic future and the credibility of institutions. As we explained in this year’s In Gold We Trust report, fundamental economic upheavals have often led to currency crises and even currency reforms. Historical developments never repeat themselves congruently, but they usually show striking similarities in terms of their causes and their sequences.[20] However, one must also be able to recognize and interpret these signs of the times.

For investors, the coming years will undoubtedly be challenging. We look forward to continuing to analyze what is happening for you and to sharing our thoughts with you. Together, we will overcome these challenges. Because for us, today more than ever in this time of profound monetary climate change:

IN GOLD WE TRUST

[1] See Nixon, Richard: “Address to the Nation Outlining a New Economic Policy: ‘The Challenge of Peace’”, The American Presidency Project, August 15, 1971

[2] “Articles of Agreement of the International Monetary Fund”, Article 2.b., p. 18

[3] “Ron Paul questions Alan Greenspan at monetary policy hearing (2002)”, YouTube, March 25, 2011

[4] See ECB: Strategy Review

[5] See Ilzetki, Ethan: “Rethinking the ECB’s inflation objective”, voxeu.org, November 16, 2020

[6] See “Portfolio characteristics: gold as an equity diversifier in recessions”, In Gold We Trust report 2019

[7] The Buffett indicator is a valuation multiple that compares the capitalization of the US Wilshire 5000 Index to US GDP. The indicator recently marked new all-time highs, exceeding the 200% level in February 2021, a level that constituted “playing with fire” according to Warren Buffett.

[8] See Wikipedia: Guns versus butter model

[9] See Market Intelligence Report, Larry Jeddeloh, May 7, 2021

[10] “WIN” buttons immediately became objects of ridicule; skeptics wore the buttons upside down and explained that “NIM” stood for “No Immediate Miracles”, “Nonstop Inflation Merry-go-round” or “Need Immediate Money”. See Wikipedia: Whip inflation now

[11] See “The Boy Who Cried Wolf – An Inflationary Decade Ahead?”, In Gold We Trust special, November 30, 2020

[12] See “Gold & Bitcoin: Stronger Together?”, In Gold We Trust report 2019

[13] See “Quo vadis, aurum?”, In Gold We Trust report 2020

[14] Option strategy consisting of two short calls at a specific strike and one long call each with a symmetrical strike above or below it.

[15] December gold options on the CME as of May 15, 2021

[16] The underlying expiration month of the options with which the calculations were performed is therefore December 2021.

[17] Due to the 50 strike rhythm, the 52-week high and low have been adjusted to the nearest 50 digits. The exact 52-week high on a closing price basis is currently USD 2,063, while the 52-week low is USD 1,681.

[18] It should be noted that the distribution varies slightly to moderately depending on the degree of exponential smoothing. In practice, a smoothing constant α of 0.1-0.3 is applied, since with a higher constant the desired smoothing is not achieved, and with a lower constant the exponential factor distorts the distribution function too much. Due to this, we decided to perform and publish the calculation of the distribution density function with all relevant expression options, i.e. without smoothing as well as with smoothing using α = 0.1, α = 0.2, and α = 0.3, to achieve the most informative and transparent results possible.

[19] See Dalio, Ray: “The Changing World Order”, LinkedIn, March 25, 2020

[20] See “3. Währungen und Werte” (“3. Currencies and Values”), Studienreihe, Donner & Reuschel, February 24, 2021