Introduction: of Wolves and Bears

“To ignore the warning signs and continue with the strategies of the past is to ignore the third, crucial cry of wolf.”

“The Boy Who Cried Wolf: Inflationary Decade Ahead?,” Incrementum Inflation Special, November 2020

Key Takeaways

- In our special analysis from the fall of 2020, „The Boy Who Cried Wolf“, we warned urgently of the underestimated danger of high inflation. The wolf is now here to stay. The war in Ukraine is exacerbating the inflation dynamic.

- The intractability of supply chain issues, the cost of sanctions, tighter monetary policy, and deglobalization are now bringing the recession bear to the table alongside the wolf.

- The majority of investors have been caught on the wrong foot by entering the inflationary environment. Balanced portfolios have been suffering heavy losses so far this year.

- In addition to de-globalization and decarbonization, there are a number of other structural reasons that argue for a longer-term stagflationary environment in which multiple waves of inflation are likely to occur.

- The freezing of Russian foreign exchange reserves and the new geopolitical realities make gold increasingly attractive as a neutral international reserve asset.

Of Wolves and Bears

In the fall of 2020, in the midst of the second Covid-19 wave, we were prompted to publish a special edition of the In Gold We Trust report. In our publication entitled “The Boy Who Cried Wolf: Inflationary Decade Ahead?”, we used Aesop’s parable to issue an urgent warning about the danger of inflation creeping up on us. The majority of market participants were no longer familiar with this predator, which was thought to be extinct, since the last period of high inflation was many decades ago.

Now the wolf is here – and it dominates the headlines. But many investors are still unaware of the threats it poses to their portfolios. In many cases, people hide behind the naïve illusion that the wolf will disappear again after a short time – just like that, and without having feasted on any prey.

Now the next danger is already lurking: sneaking up behind the wolf is a bear. This bear symbolizes a striking economic downturn, pushing asset prices down with its paw. Once again, the majority of economists and investors will be caught on the wrong foot.

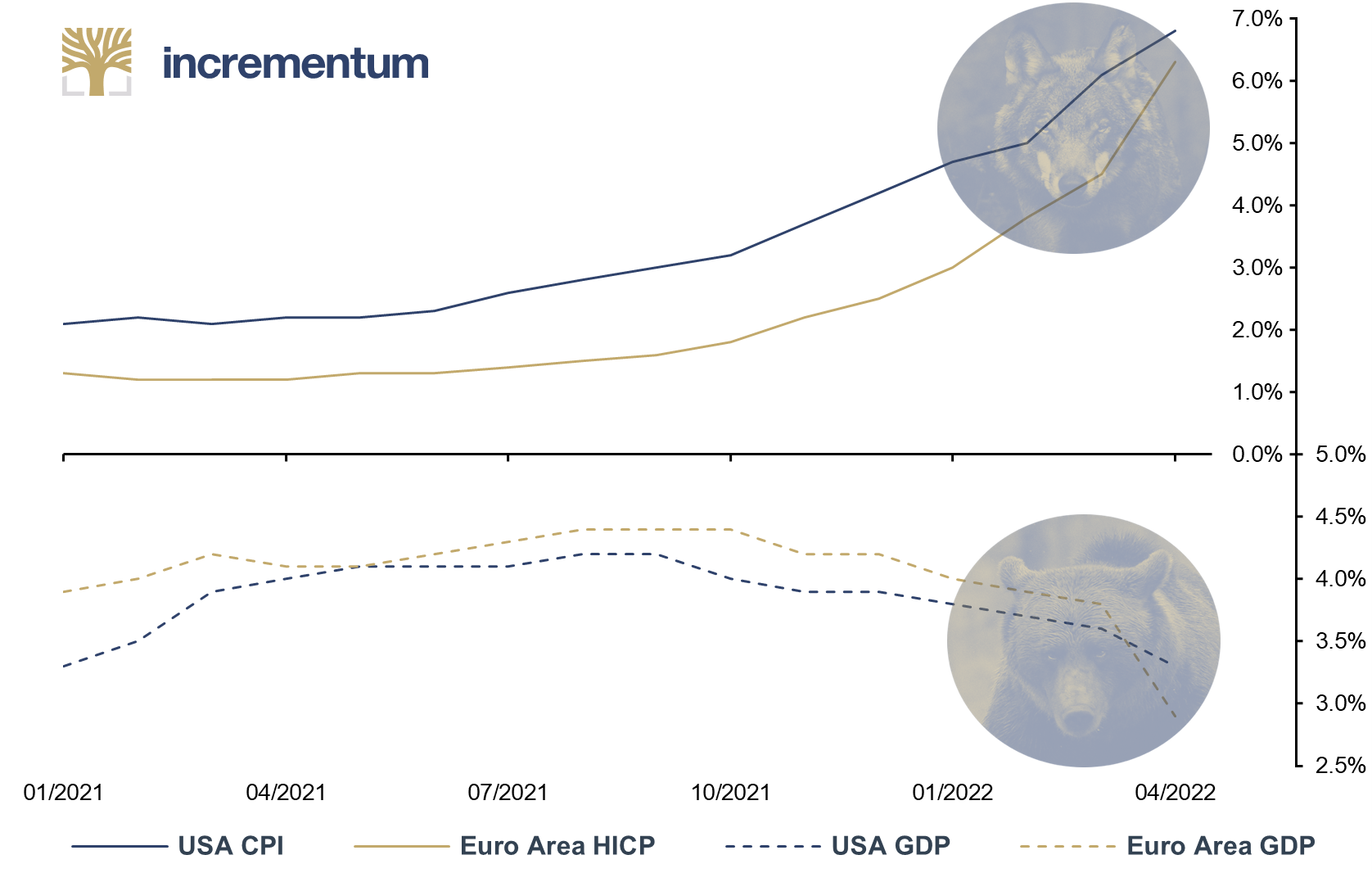

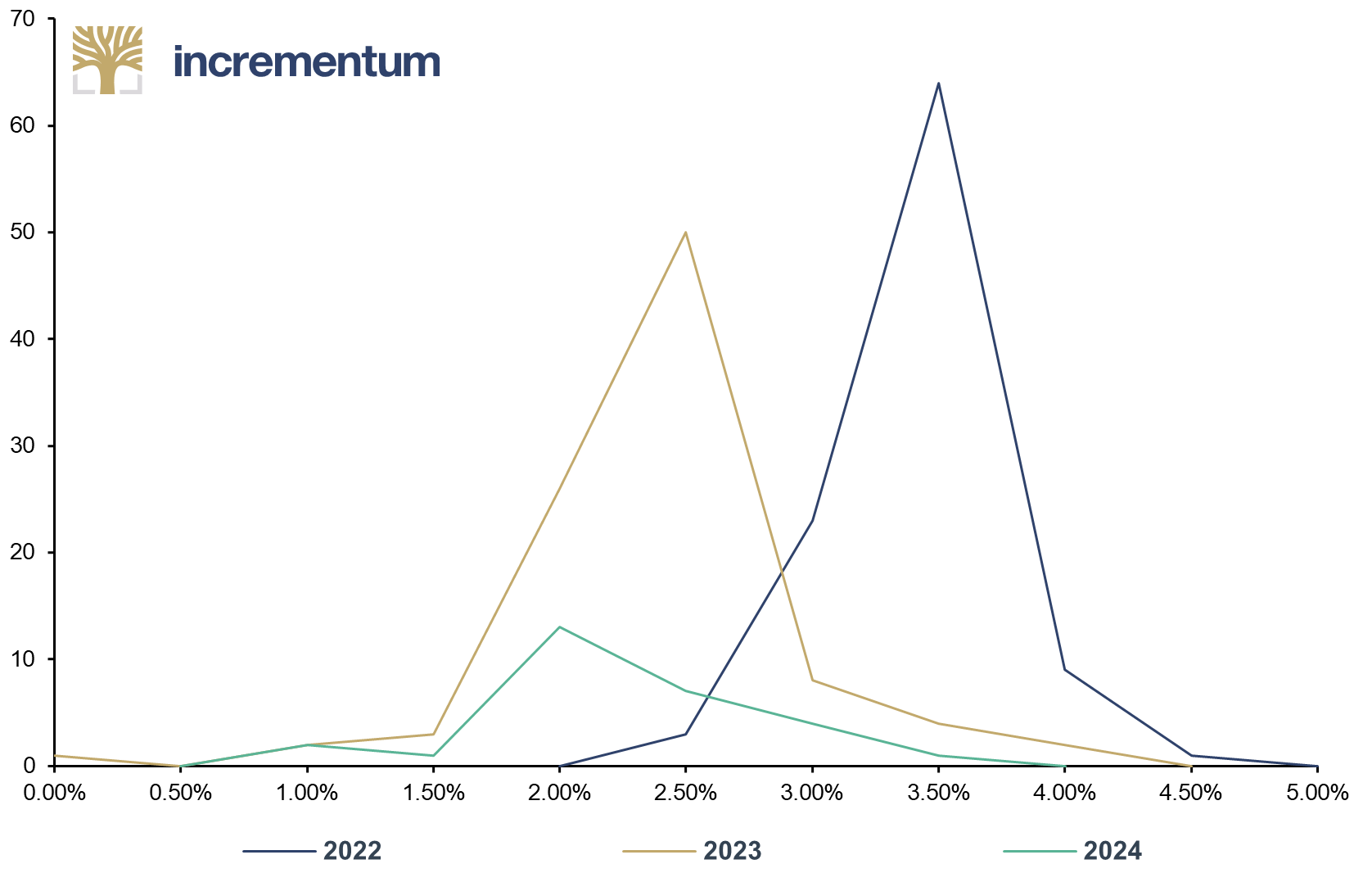

Monthly Inflation and GDP Polls for 2022, USA and Euro Area, 01/2021-04/2022

Source: Reuters Eikon, Incrementum AG

After the devastation of the Covid-19 pandemic, everyone hoped for years of recovery. Last year’s record-high growth figures fueled this fire of hope. But these figures were mainly due to a return to a certain economic normality dependent on the base effect.

But what was the real tinder that caused this growth fire to burn? In the wake of the global lockdowns and the equity market crash, the US economy contracted by an annualized 9.1% in Q2/2020, while global GDP slumped by 3.1%. An unprecedented flurry of monetary and fiscal policies were implemented in an attempt to limit the economic damage caused by the lockdowns and prevent the looming debt-deflation.

The stock markets reacted with delight, deflation was averted, and just a few months later the financial markets were once again in high spirits. The S&P 500 rallied from its Covid-19 low to a new all-time high in just 5 months, and the Nasdaq soared 134% from low to high in just 3 months.

But the inflationary side effects of the brute monetary and fiscal revival measures manifested themselves quietly over the course of the past year. The price paid for rescuing the markets was steadily rising inflation, which broke through the central banks’ 2% target in both the US and the euro area in mid-2021.

But central bankers appeased us. Don’t be afraid of the wolf; the howl you think you hear is just your imagination; the surge in inflation is merely transitory. Consequently, this appeasement was also to be found in institutions’ inflation forecasts. The ECB’s inflation forecast is exemplary for its dramatic misjudgment of the situation. In September 2021, an inflation rate of 1.7% was projected for 2022; in December 2021, the forecast was raised to 3.2%; and in March it had climbed to 5.1%. Even before the outbreak of the Ukraine war, the ECB almost had to double its inflation forecast within the span of three months.

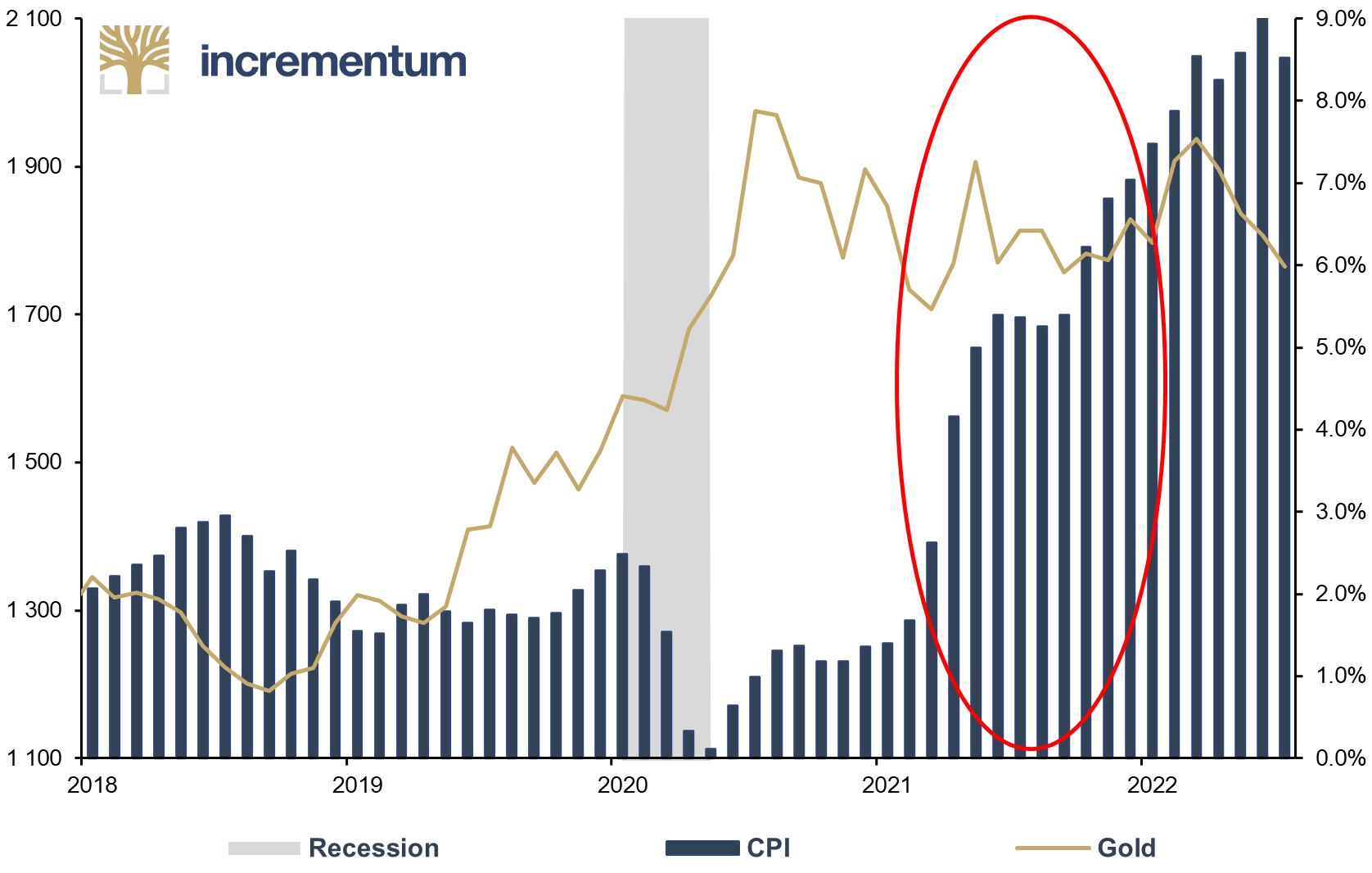

Initially, the gold price reacted disappointingly to the inflation increase of the previous year. Over the course of 2021, gold holders had to settle for a modest return of +3.6% in EUR or -3.5% in USD.

Gold (lhs), in USD, and CPI (rhs), 01/1970-04/2022

Source: Reuters Eikon, Incrementum AG

The reasons why gold temporarily lost its mojo were:

- A strong prior performance: 2019: +18.3% (USD), +21% (EUR); 2020: +24.6% (USD), +14.3% (EUR)

- The extremely firm US dollar

- High opportunity costs because of soaring stock markets

- Crypto assets that stole the show from gold

- Most importantly, market participants believed the transitory narrative and did not fear that inflation would remain high in the longer term.

The longer inflation stayed elevated, the more market participants thought that this must affect the price of gold. It was not until the beginning of 2022 that the price gradually began to react to the increased inflation and the growing turbulence on the stock and bond markets.

The Russian Bear

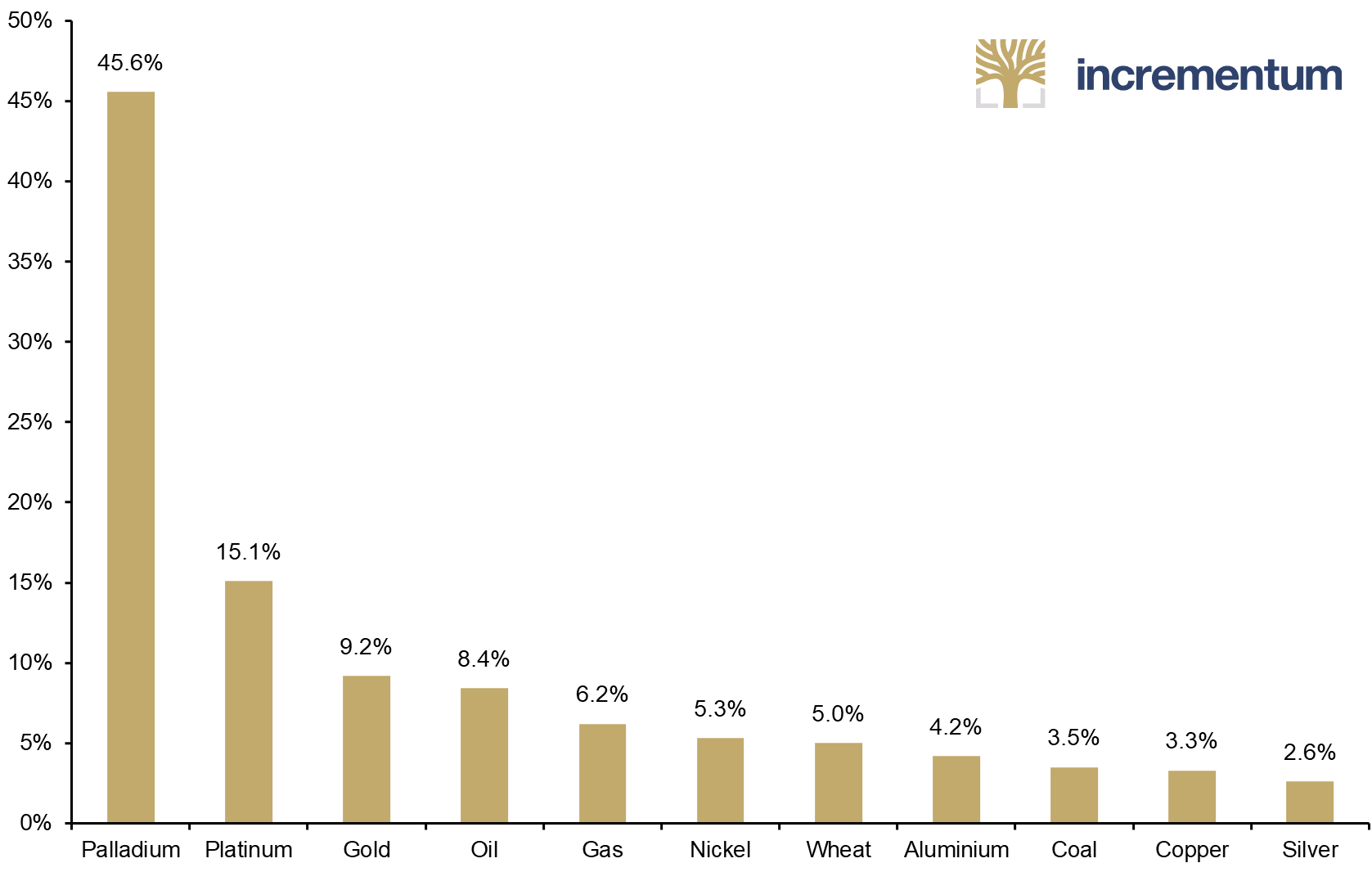

It is obvious that Russia’s attack on Ukraine will have a further exacerbating effect on the inflation situation. Russia is one of the major exporters of raw materials, not only in the energy sector. However, what we believe is severely underestimated is the disastrous cost to national economies faced with the substitution of Russian resources. German Minister for Economic Affairs Robert Habeck put it succinctly in a discussion on a possible EU oil embargo against Russia: “This cannot be had without any pain!” JP Morgan estimated in mid-April that an oil embargo would send the price of oil soaring to USD 185. That would be a jump of another 70-80% or so. One does not need to be a great prophet to predict the impact of such a price jump on the economy and inflation rates. The sanctions spiral will certainly cause not only the wolf but also the bear to run rampant.

Russia’s Exports, as % of Global Production, 2021

Source: Bloomberg, JPMorgan, Incrementum AG

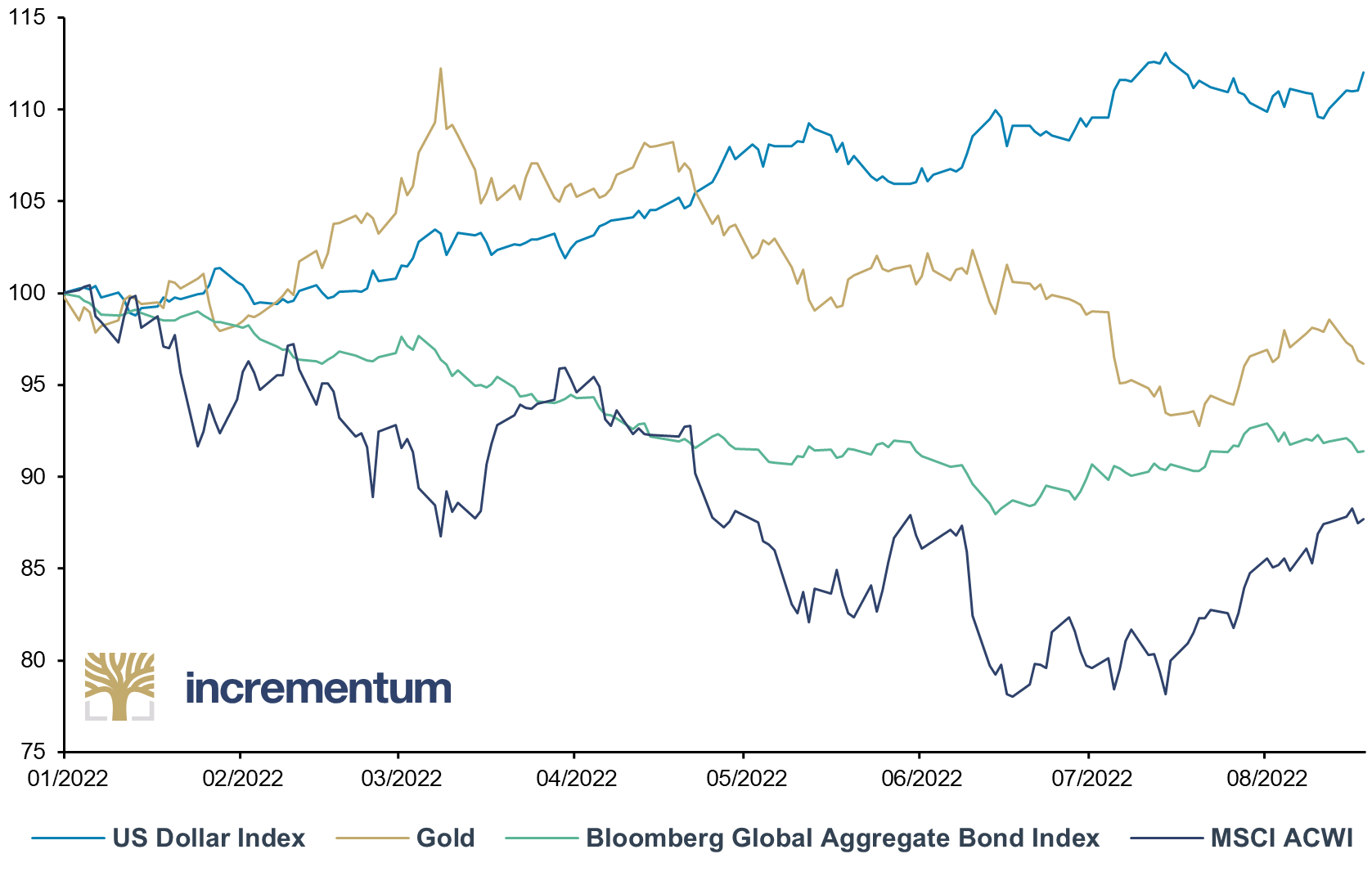

And that bear can already be seen prowling the capital markets. The S&P 500 dropped more than 15% since the beginning of the year, while the Nasdaq is down 25%. The bears have reached the former epicenter of the US bull market: the vaunted technology stocks. But the ursine brute is also loose in the bond markets. In Q1/2022, US Treasury bonds posted their worst performance since records began in 1973, according to the Bloomberg US Treasury Total Return Index. And also in the currency markets the bear has appeared, the US Dollar Index climbed to its highest level since 2002. Gold held up well in this adverse environment, but lost its strength from mid-April onwards.

US Dollar Index, Gold, Bloomberg Global Aggregate Bond Index, and MSCI-ACWI, in USD, 100 = 31.12.2021, 01/2022-05/2022

Source: Reuters Eikon, Incrementum AG

The bear is also slowly making its presence felt in economic terms. In Q1/2022, the USA probably already recorded a decline in economic output. After annualized quarterly growth of 6.9% in Q4/2021, the economy contracted by 1.4% in Q1/2022 according to the latest GDP estimate of the Bureau of Economic Analysis (BEA), even though the initial estimate was for over 3% growth. Even if growth in the current quarter is again slightly positive and a (technical) recession can still be avoided for the time being, a recession in the next 12-18 months is much more likely than currently assumed by economists and the market.

US GDP Polls, Annual GDP Growth (x-axis), and Number of Analysts (y-axis), 04/2022

Source: Reuters Eikon, Incrementum AG

The Momentous Freeze of Russian Foreign Exchange Reserves

The status of the US dollar as the global reserve and trade currency is showing unmistakably widening cracks. For many years now, we have been documenting the process of de-dollarization. We are now eyewitnesses to a momentous breach of confidence that is preparing the ground for a move away from the US dollar as the world’s reserve currency and, in the medium term, accelerating the path to a new global monetary order.

The decision of the G7 and the EU on February 26 to freeze the US dollar and euro currency reserves of the Russian Central Bank, which account for about 60% of its total international reserves, will go down in monetary history. Although there have been sanctions against pariah states such as Venezuela, Iran, or the Taliban’s Afghanistan before, they have never before been applied against a state with veto power in the UN Security Council, a former member of the leading economic nations (G8), a nuclear power, and one of the world’s most important exporters of raw materials.

With the weaponization of money, however, the US and the EU are unlikely to have done themselves any favors in the medium to long term. The decision clearly demonstrates to many US-critical nations how quickly US dollar reserves can transform from a highly liquid asset to useless pieces of printed paper. De facto, the US and the euro area have told the world that they no longer want to pay their economic quid pro quo from previous trade deals.

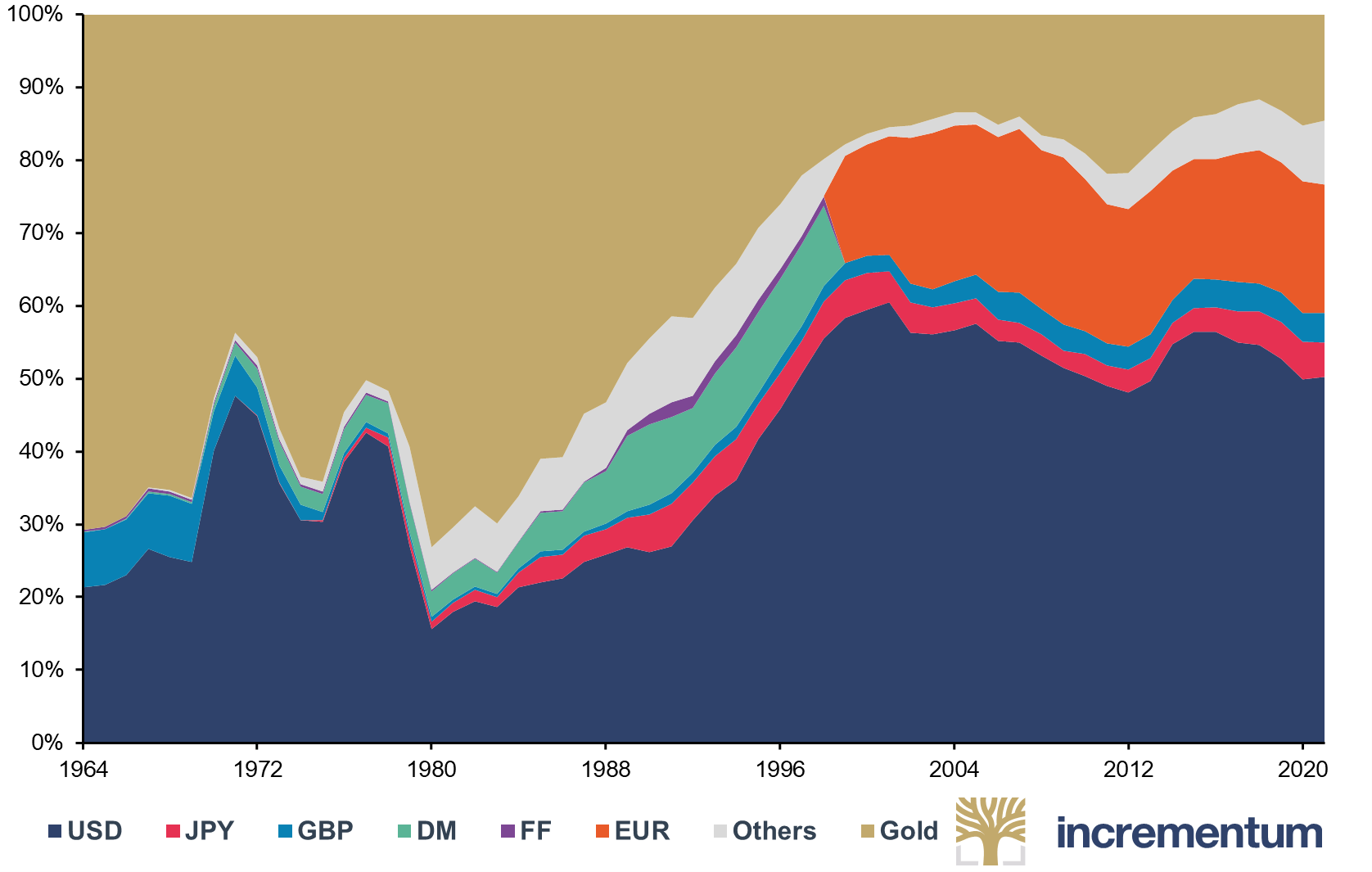

Composition of Global FX Reserves incl. Gold, 1964-2021

Source: IMF, World Gold Council, Incrementum AG

The volume we are talking about is enormous: The global foreign exchange reserves of central banks amount to around 12trn USD, of which the US dollar accounts for about 60% and the euro for 20%. China, in particular, will have been watching Russia’s reserve freeze with a wary eye and will be stepping up its efforts toward monetary sovereignty. In addition, the freezing of currency reserves has a potentially strong deflationary effect.

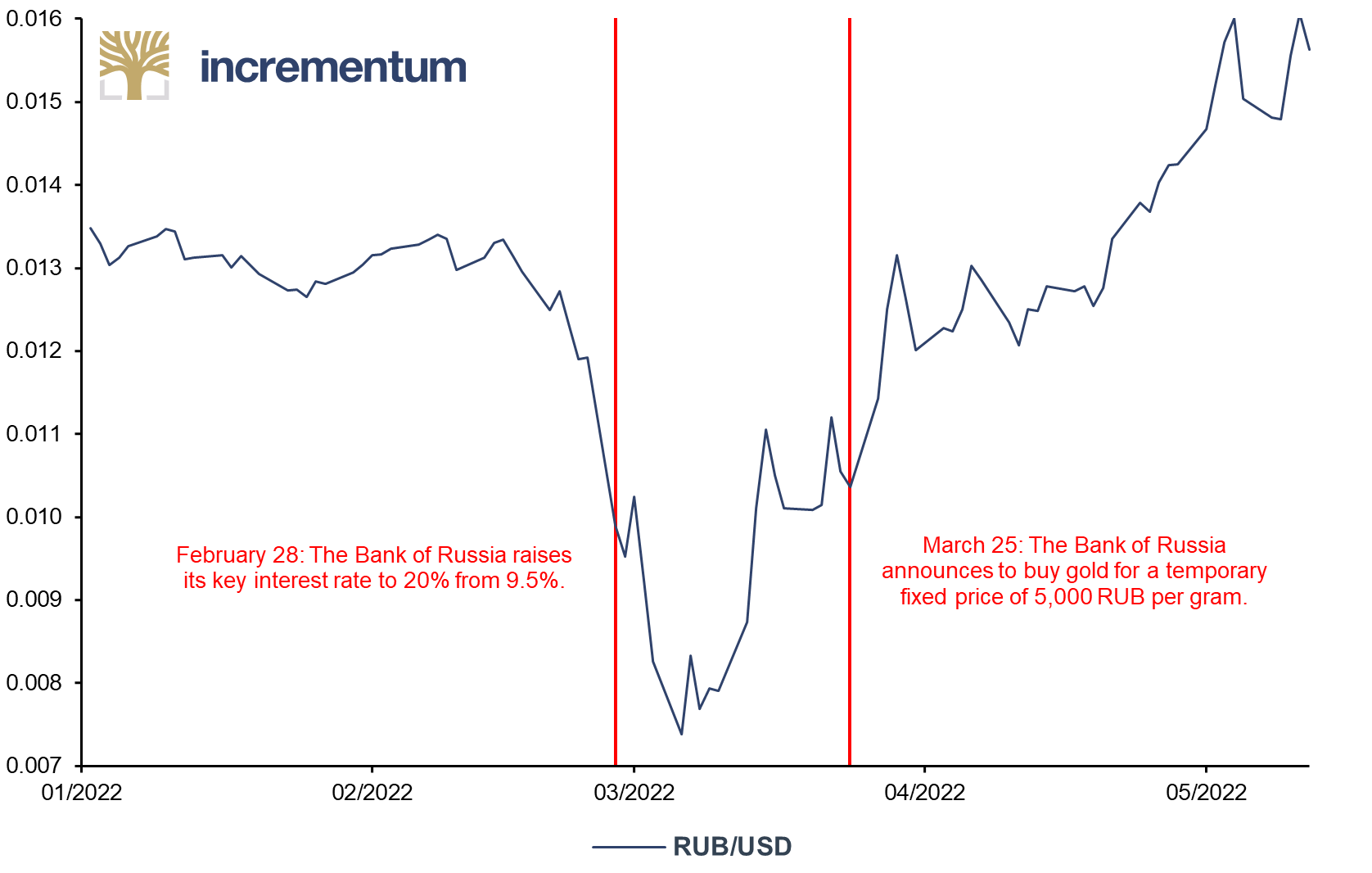

Remarkable countermeasures were taken to support the collapsing ruble. For example, the Russian Central Bank – after doubling its key interest rate to 20% – announced that it would pay a fixed price of 5,000 rubles per gram of gold from March 28 until June 30. This is equivalent to about USD 1,940 per ounce. This establishes a floor for the gold price in rubles, and since gold is traded in US dollars, it also implicitly establishes a floor for the ruble in US dollars.

Some analysts have mistakenly referred to this mechanism as the new gold standard. However, this is not the case, as the central bank has not committed itself to redeeming rubles for gold, but only issues rubles and accepts gold. Nevertheless, this example illustrates most vividly that gold can be used at any time not only as a proverbial but as an actual anchor for a fiat currency.

What is extremely impressive is how the external value of the ruble has developed against the US dollar, which is itself extremely strong. For example, the ruble is trading firmer against the US dollar than at the beginning of the year, despite six waves of tough sanctions already in place.

RUB/USD, 01/2022-05/2022

Source: Reuters Eikon, Incrementum AG

In addition to the gold price floor, the decision that Russia will no longer accept euros as a means of payment for its exports is likely to have played a significant role in the unexpected strength of the ruble. The chairman of the energy committee in the Russian Duma, Pavel Zavalny, commented on the Russian decision to no longer accept the euro as a means of payment: “Let them pay either in hard currency, and this is gold for us, or pay as it is convenient for us, this is the national currency.” (Our emphasis.) From the states classified as unfriendly Russia will in future only accept payment in rubles or in gold, and from all others in a freely negotiable currency and possibly even in Bitcoin.

We are concerned that the West may be overestimating its position with regard to its de facto monopoly on international currency reserves. The economic importance of the East – especially Asia – has increased massively over the past 20 years. This power has been highlighted by Sergey Glazyev. He is considered one of Russia’s most influential economists and is a member of the National Finance Council and former Minister of Foreign Economic Relations. He was also an economic advisor to President Putin from 2012-2019. Glazyev explained the role that commodities will play in the emerging multipolar monetary order:

“The third and the final stage on the new economic order transition will involve a creation of a new digital payment currency… A currency like this can be issued by a pool of currency reserves of BRICS countries… the basket could contain an index of prices of main exchange-traded commodities: gold and other precious metals, key industrial metals, hydrocarbons, grains, sugar, as well as water and other natural resources…”

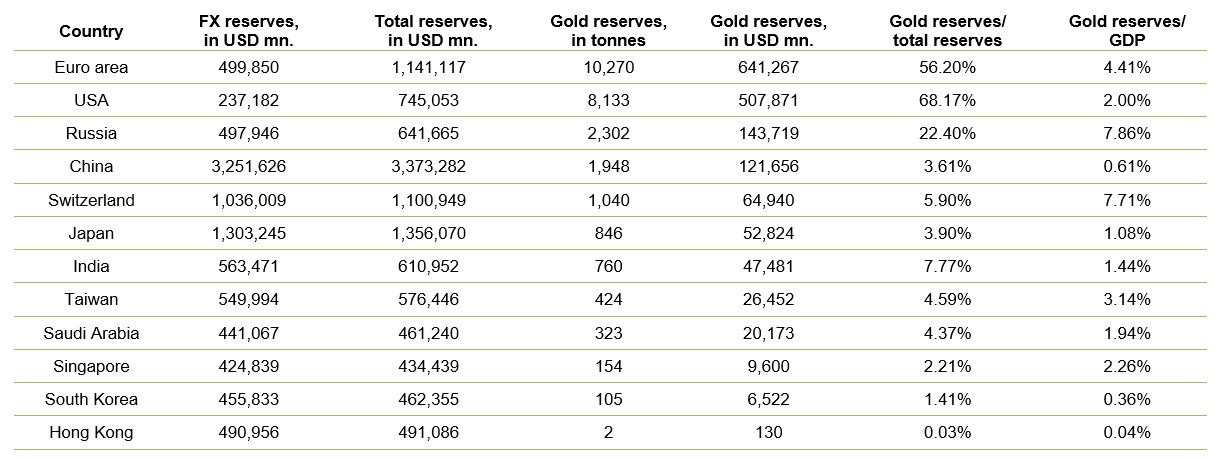

We think it is plausible that gold, as a neutral monetary reserve, will emerge as one of the beneficiaries of the troubling conflict between East and West. In an increasingly polarized world that is dividing into two blocs, gold can act as a neutral, nonstate monetary intermediary. Meanwhile, the trend of gold enjoying increasing popularity among central banks has continued unabated since 2008. Thus, while the BRICS countries have significantly increased their gold reserves in recent years, the West, especially the euro area and the US, is still well ahead in this ranking.

Source: IMF, World Gold Council, Incrementum AG (data as of Q1/2022).

In addition to the unique feature that gold has no risk of default or confiscation – provided it is held securely in the country that owns it – central banks now have another argument in favor of holding reserves in gold. Inflation rates, which are markedly beyond their respective inflation targets, are likely to further undermine confidence in government reserve currencies in the coming years. Gold will probably gain further acceptance as a reserve currency in many countries and increasingly establish itself as an anchor of confidence and purchasing power.

Even though Bitcoin was mentioned in passing by Russia in this context – which is remarkable – it does not play a role in the concert of reserve currencies at present. However, in the oldest of all cryptocurrencies adaptation continues to progress steadily. Worth mentioning, in addition to the integration of Bitcoin as an asset into traditional financial markets, is the increasing use of the protocol for processing payments via the Lightning Network.

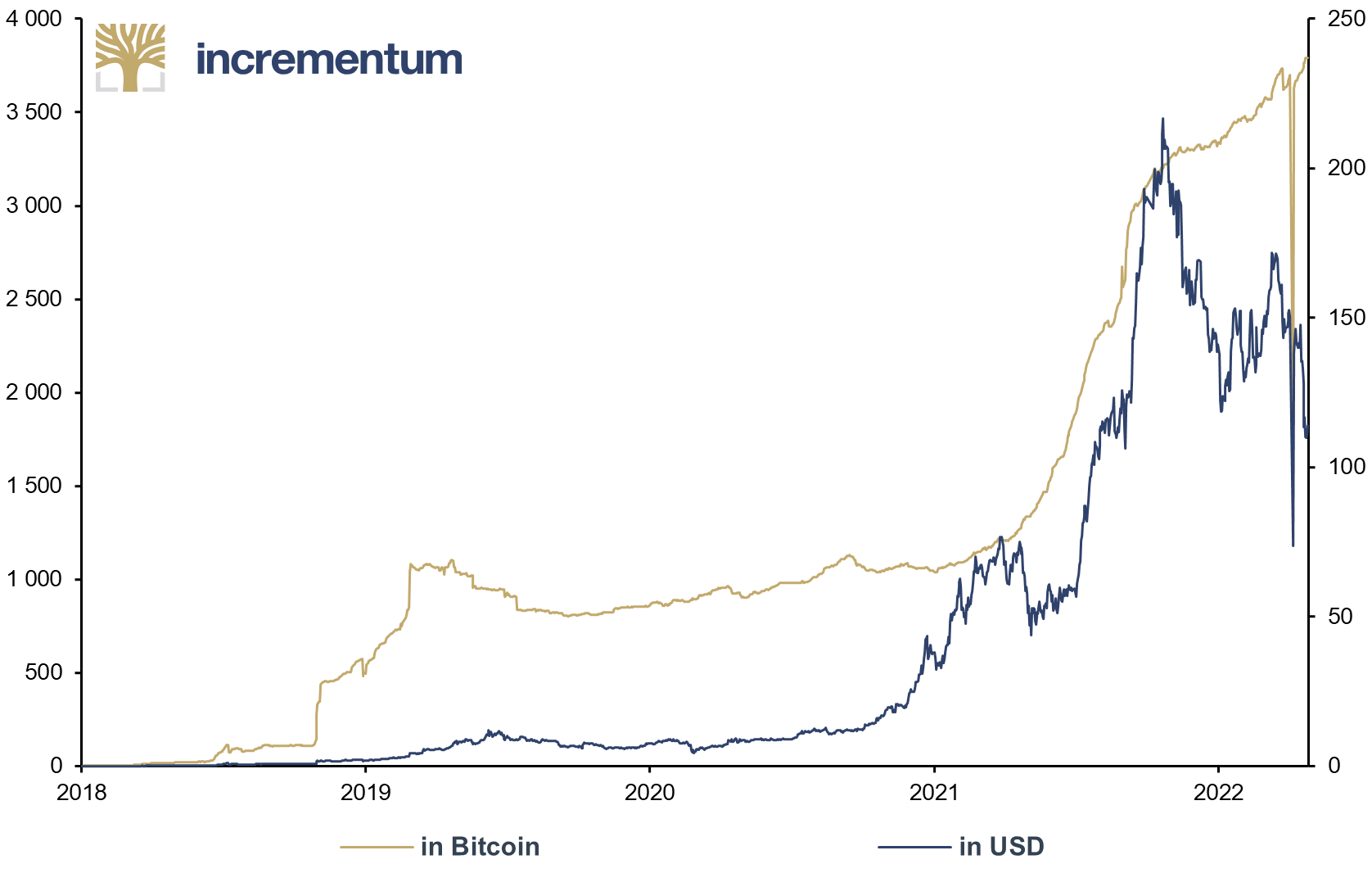

Lightning Network Capacity, in Bitcoin (lhs), and USD (rhs), 01/2018/05/2022

Source: bitcoinvisuals.com, Incrementum AG

Bitcoin is being discovered by a growing part of the population in developing countries and is also being actively used as a means of payment. Thus, a bottom-up dynamic can be seen here. Central banks, on the other hand, still want nothing to do with the decentralized digital currency. But even so, there are always interesting initiatives. For example, at the April 2022 general meeting of the SNB, a request was made by some of the bank’s shareholders that it should shift 1 billion francs of its assets per month from Eurobonds into Bitcoin.a request was made by shareholders As expected, the request was not favored by the central bank. Consequently, the initiators will probably confront the SNB with the issue every year from now on.

But there are also newsworthy developments at the state level with regard to Bitcoin: Last year, El Salvador introduced Bitcoin as an official means of payment alongside the US dollar. The Central African Republic has recently followed suit. In both cases, the IMF opposed the moves vociferously and warned of considerable risk. That institution, which forbids its member states from pegging their currencies to gold, is obviously strongly opposed to Bitcoin becoming official money. One cannot escape the impression that the IMF is, at its core, the supreme guardian of the global debt-based monetary system.

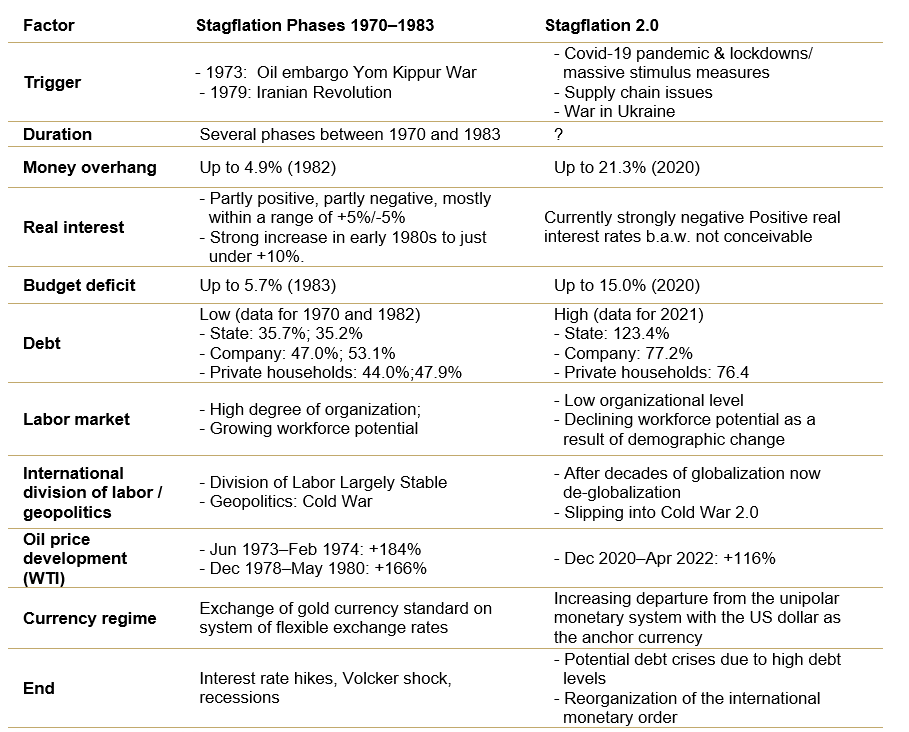

From Monetary Climate Change to Stagflation 2.0

Before we turn to our core topic this year, stagflation, allow us to take a quick look in the rearview mirror. In the In Gold We Trust report 2021 we talked about what we called monetary climate change. With this term, we alluded to a multilayered paradigm shift triggered by the pandemic and the political reactions to it, and shaped by the following five developments:

- Budgetary nonchalance

- Merging of monetary and fiscal policy

- New tasks for monetary policy

- Digital central bank currencies vs. decentralized cryptocurrencies

- The new ice age between East and West

These trends are still present and are further reinforced by the Russian crisis. The budgetary nonchalance continues seamlessly after the Covid-19crisis has abated. No expense is being spared to develop alternative energy sources, to massively rearm and to finance the costs of sanctions, but also to cushion the wave of inflation through transfer payments. Monetary policy will have no choice but to finance the additional government budget gaps by monetizing public debt. Relations between East and West have cooled down so much that one can already speak of a Cold War 2.0. These are all structurally inflationary dynamics, which have a braking effect on growth on top of everything else.

Wolf and bear, inflation and economic downturn equals stagflation.

This is precisely the insight that is slowly but surely taking hold. No less a person than the president of the renowned German ifo Institute, Clemens Fuest, already surprised us at the end of April (!) with the following statement: “We are in the midst of stagflation, at least in Europe.” In view of the tense geopolitical situation and the dark clouds in the economic sky, we consider stagflation to be very likely in many parts of the world, especially in the USA and the EU.

Just as we predicted the current wave of inflation in 2020 without going far out on a limb, we are also not going out on a limb with our announcement of persistent stagflation. We will certainly not have to endure a repeat of the stagflation of the 1970s; rather, we’ll see stagflation 2.0, with its numerous peculiarities. We will compare some of the important characteristics here with a focus on the US.

Source: Incrementum AG

Stagflations and their consequences for the economy, society and financial markets are probably only known to most people from history books, if at all. Adequate preparation for the simultaneous appearance of wolf and bear, which is even rarer to observe than a German victory in the song contest, will occupy us in all its details in this year’s In Gold We Trust report.

Thank you very much!

Year after year, the In Gold We Trust report strives to be the world’s most recognized, widely read, and most comprehensive analysis on gold. We wholeheartedly thank our more than 20 fantastic colleagues on four continents[1] for their energetic and tireless efforts!

Our thanks also go to our premium partners, of course.[2] Without their support it would not be possible to make the In Gold We Trust report available free of charge and to expand our range of services year after year. In 2022, for example, we launched our Monthly Gold Compass as well as a Spanish edition of the compact version.

Studying and appreciating the past is crucial to preparing for the future. Understanding and preparing for the monetary climate change described last year[3] as well as Stagflation 2.0 are, in our opinion, key analytical challenges of the present. We are pleased to once again provide you, dear readers, with a comprehensive, informative and entertaining guide to gold.

Now we invite you on our annual parforce ride and hope you enjoy reading our 16th In Gold We Trust report as much as we enjoyed writing it.

With warm regards from Liechtenstein,

Ronald-Peter Stöferle and Mark J. Valek

[1] All employees are pictured in the employee gallery at the end of the In Gold We Trust report.

[2] At the end of the In Gold We Trust report you will find an overview of our Premium Partners, including a brief description of the companies.

[1] “Monetary Climate Change,” In Gold We Trust report 2021