Introduction

“An idea is like a virus. Resilient. Highly contagious. And even the smallest seed of an idea can grow. It can grow to define or destroy you.”

Dominic Cobb, Inception

Key Takeaways

- This year marks the 50th anniversary of the Nixon Shock when the last peg between money and gold was severed. This event ushered in the era of debt-based money and allowed central banks to create money without restrictions.

- A monetary climate change is taking place right before our eyes. We identify three key aspects to this change: budgetary nonchalance, the merging of monetary and fiscal policy and the creation of new tasks for monetary policy.

- In our view, the inflation pendulum finally swung back in the previous year, and inflationary forces are now stronger than deflationary ones.

- We are likely moving into a period of inflation caused by strongly rising money supply growth. Consequently, more and more central banks will be forced to implement a policy of explicit or implicit yield curve control. Real interest rates will thus remain negative.

- We maintain our forecast based on our proprietary gold price model presented last year. The conservative baseline scenario has resulted in a price target of USD 4,800 for gold at the end of the decade.

- After hibernating for years, commodity prices have now awakened. In such a market environment, tangible assets, especially commodities, selected equities in the right sector, and obviously precious metals should form the solid basis of the portfolio.

Climate change and the associated striving for a “more sustainable economy” are omnipresent issues today. From energy production and mobility to the food industry and retail, to government bonds and investment funds, everything imaginable is given predicates such as “green”, “sustainable” or “climate-neutral”. ESG [1] and SRI [2] have become winged acronyms that no one seems able to elude.

Of course, efforts aimed at structural improvement in the areas of environment, social affairs, and corporate governance are welcome. From our point of view, however, the considerations have a serious shortcoming. They do not include the foundation of the current economic system in their consideration: the debt-based monetary system.

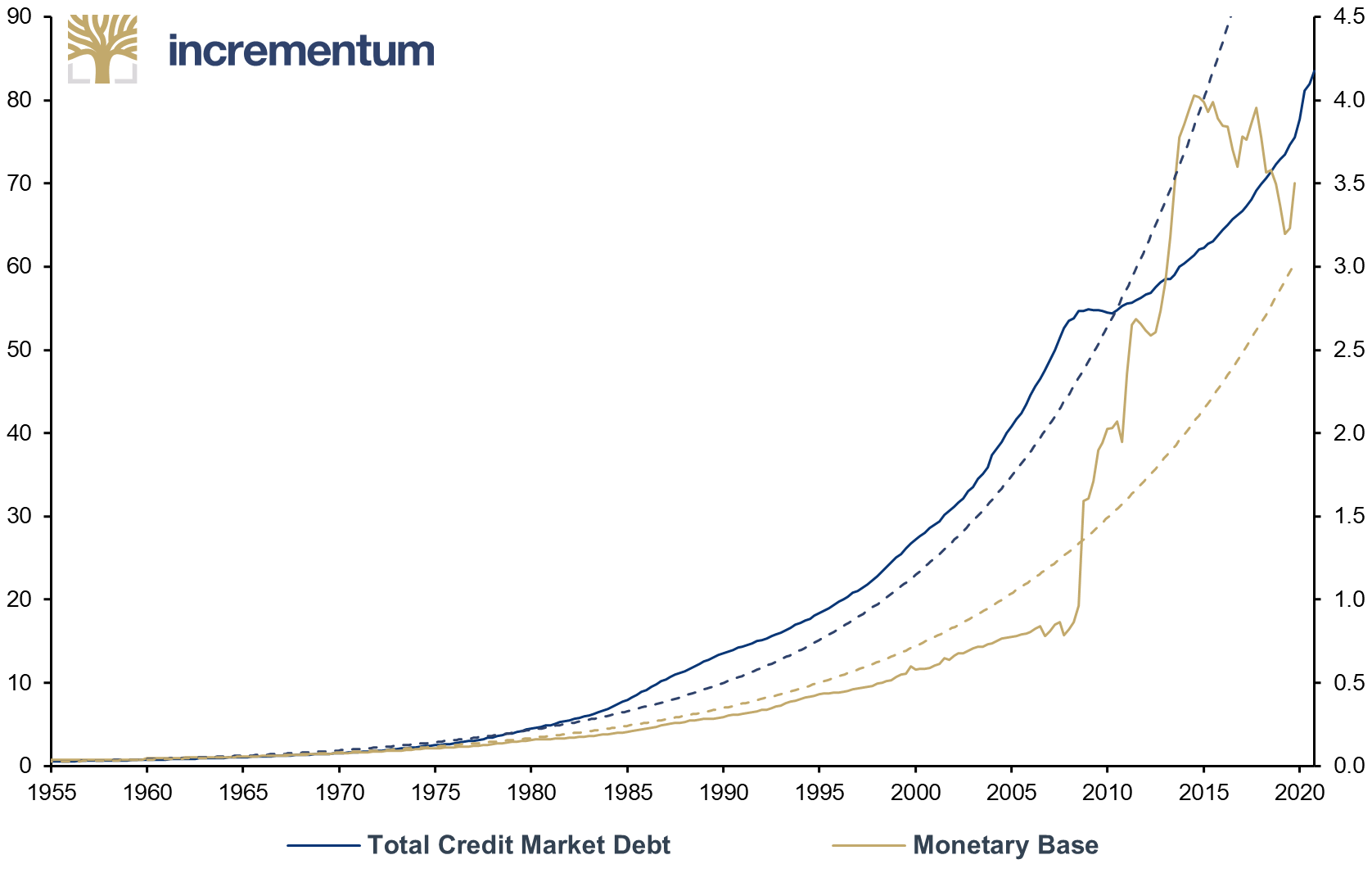

This year marks the 50th anniversary of its birth – ironically, the final separation of the world monetary system from gold will celebrate its golden wedding in a few weeks. As our loyal readers know, the last peg of the US dollar to gold was severed on August 15, 1971, which completely dematerialized the global monetary system. Since then, no currency has been backed by a scarce asset like gold. Central banks can create money without any restrictions and are increasingly making use of this privilege. Various money supply and debt aggregates have been rising exponentially ever since.

Total Credit Market Debt (lhs), in USD trn, and Monetary Base (rhs), in USD trn, Q1/1955-Q4/2020

Source: Reuters Eikon, Incrementum AG

In the In Gold We Trust report 2019, our leitmotif was trust.[3] Currencies are based on a triad of stability, credibility and confidence.[4] In our opinion, this trust in the future purchasing power of money is on the brink of collapse, as currently evidenced by the crack-up boom-like developments in the financial markets. Ultimately, the public’s trust in unbacked currencies stands or falls on whether central banks do not abuse the money-creation privilege, for example for covert government financing. But it is precisely in this context that we are registering those fundamental changes that, taken together, paint the picture of a monetary climate change.

What exactly do we mean by monetary climate change? We are alluding to a multilayered paradigm shift, the breakthrough to which was triggered by the pandemic and the political reactions to it. The following developments are an expression of this profound change:

1. Budgetary nonchalance

Fiscal conservatism has been in retreat for some time. In the euro area, the credo of the frugal Swabian housewife still prevailed in the aftermath of the Greek crisis – especially at the instigation of Germany. But since the onset of the pandemic, governments have embraced their role as big spenders more enthusiastically than ever. Whether it is debt-financed subsidies for “green” companies or permanent transfer payments to ever larger parts of the population, there are more and more goals that are seen as so important that higher debt is accepted for them. The ultimate constraints, such as the US debt ceiling, the Maastricht criteria of the European Union, and other national debt brakes are suspended, interpreted generously, or simply ignored – après nous le déluge. This permissive fiscal zeitgeist also has significant implications for monetary policy.

2. Merging of monetary and fiscal policy

This new fiscal dominance is accelerating the merging of monetary and fiscal policy. Emblematic of this is the appointment of former Federal Reserve Chair Janet Yellen as US Treasury secretary and former ECB President Mario Draghi as Italian prime minister. Even the central bank governors of the former hard-currency countries in the euro zone are now encouraging the responsible budget politicians to run even higher deficits.[5] Consequently, a successively higher share of the deficits must be financed via the digital printing press. More and more aspects of the Modern Monetary Theory[6] now seem to be subjected to a practical test. But the political independence of central banks has always been the institutional guarantor of confidence in the stability of the currency. The closer this liaison between monetary and fiscal policy grows, and the longer it persists, the greater the likelihood of a loss of confidence.

3. New tasks for monetary policy

Safeguarding price stability has always been considered the primary objective of an independent central bank. Increasingly, one gets the impression that central bankers are speaking out more often on issues such as sustainability, climate change, or diversity than on monetary policy matters. For example, ECB President Christine Lagarde, against all custom, made a public statement of support for the Green Party’s top candidate in the upcoming German federal election. The self-designation of central bankers as monetary guardians therefore seems out of date. Moreover, the criteria for price stability are being redefined in many places. The Federal Reserve has already taken this step by switching to “average inflation targeting” (AIT) in the summer of 2020, while the ECB is currently reviewing its monetary policy strategy. In our view, it is very likely that the ECB’s price stability target, which is considered sacrosanct, will be softened in the future.

4. Central bank digital currencies vs. decentralized cryptocurrencies

One aspiration of many central banks is to hastily introduce a central bank digital currency (CBDC). In our view, CBDCs are a wolf in sheep’s clothing. It seems as if the excitement around “digital assets” is being exploited to market state-owned digital currencies as a great achievement. In fact, these would enable the implementation of even deeper negative interest rates as well as permit the most extensive pushback against anonymous cash that we have yet witnessed. The advent of CBDC’s would mark a milestone on the road to the transparent citizen.[7] A recently published study by Kraken appropriately refers to digital central bank currencies as “digitized fiat currency”.[8] The antidote to CBDCs are noninflationary, decentralized cryptocurrencies, which will continue to flourish as a consequence of monetary climate change and increasingly become the focus of the mainstream.[9]

5. The new ice age between East and West

The secular divergence, especially between the US and its allies on the one hand and China and Russia[10] on the other, already existed before the pandemic but has recently accelerated. The steady cooling of diplomatic relations has had a marked impact on the economic situation of the respective states. But Europe was also divided rather than welded together by the Covid-19 crisis. Both a north-south division and an east-west division (Western Europe vs. the Visegrád states) can be observed. Monetary climate change also has far-reaching consequences at the level of international monetary policy. The quest for new trading and reserve currencies continues to grow, and de-dollarization is advancing. Gold plays a central role in this emancipation from the US dollar.

From Asset Price Inflation to Consumer Price Inflation

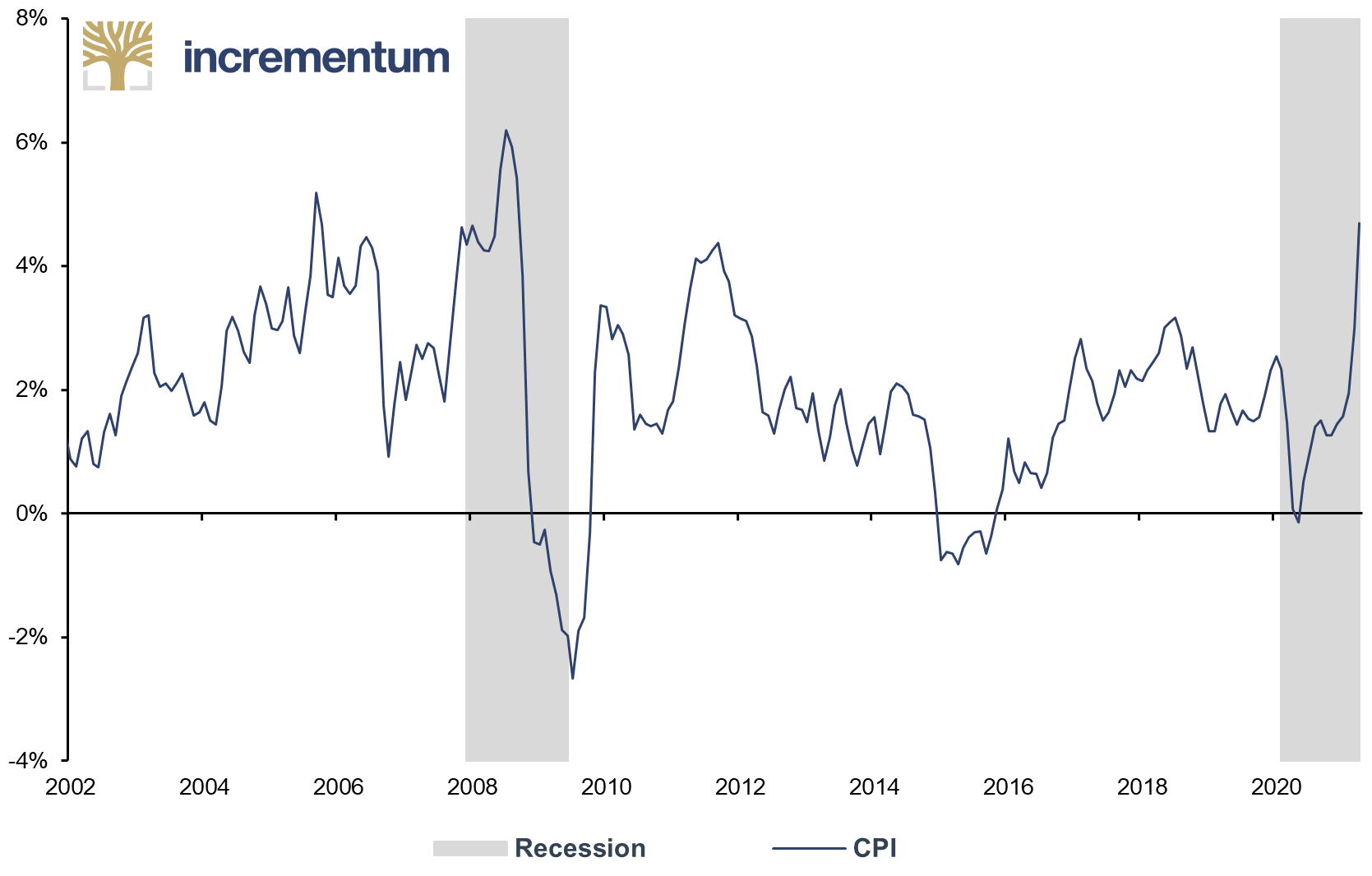

Meteorological climate change carries the risk of sea level rise. A side effect of monetary climate change is the almost unlimited wave of liquidity that has been flooding the markets since the beginning of the Covid-19 pandemic and that is already causing a noticeable increase in both asset price levels and consumer price levels. Possibly one of the most dramatic consequences that the new monetary climate could bring is the renaissance of consumer price inflation. In our opinion, we are currently only in the early stages of this inflationary development.

CPI, yoy%, 01/1960-04/2021

Source: Reuters Eikon, Incrementum AG

At the heart of the narrative of central banks regarding current inflationary dynamics is one term: temporary. For example, the most recently added member of the Federal Reserve’s Board of Governors, Christopher Waller, made the following statement: “Whatever temporary surge in inflation we see right now is not going to last.” [11] Federal Reserve Chairman Jerome Powell consistently conveys the same message. On this side of the Atlantic, ECB President Christine Lagarde is also tooting the same horn.

We look to the future with great interest and concern in the coming months and years, as it becomes clear whether the current surge in consumer price inflation is temporary or permanent.

In this context, it is worth studying the book The Tipping Point, How little things can make a big difference,[12] by Malcolm Gladwell. Gladwell defines a tipping point as “the moment of critical mass, the threshold, the boiling point”. The media regularly warn of irreversible tipping points being reached in manmade climate change. That such tipping points loom in the context of monetary climate change – a reversal of inflation expectations or even broad erosion of confidence in the monetary foundation – is not even considered by the bulk of market participants, policymakers and economists. In our view, the inflation pendulum has finally swung back in the past year, and inflationary forces are now stronger than deflationary ones.

The Boy Who Cried Wolf

In fall 2020 we were prompted for the first time to publish an In Gold We Trust special entitled “The Boy Who Cried Wolf: Is an Inflationary Decade Ahead?”.[13] Aesop’s parable describes how villagers simply ignored a renewed warning of a wolf following false alarms from a shepherd boy. Something similar is currently happening on the part of savers and investors in connection with the danger of a wave of inflation. In our special report we showed why inflationary forces are now finally gaining the upper hand. In this In Gold We Trust report, we will again look at the complex issue of inflation from different angles.

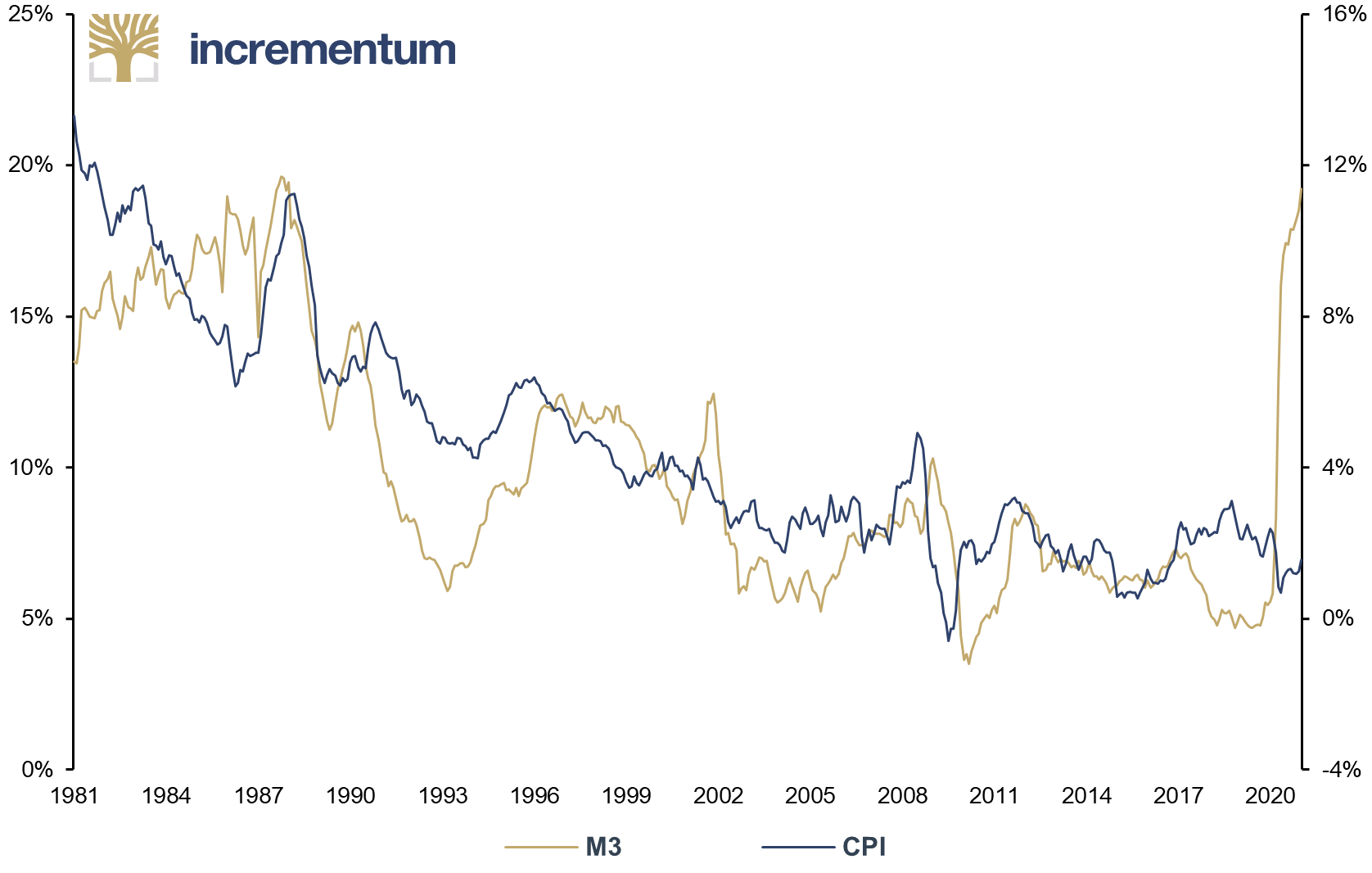

One obvious reason for strongly rising inflation rates in the coming months is the historic increase in the M3 money supply in many parts of the world.

OECD M3 (lhs), yoy%, and OECD CPI (rhs), yoy%, 01/1982-01/2021

Source: Federal Reserve St. Louis, Incrementum AG

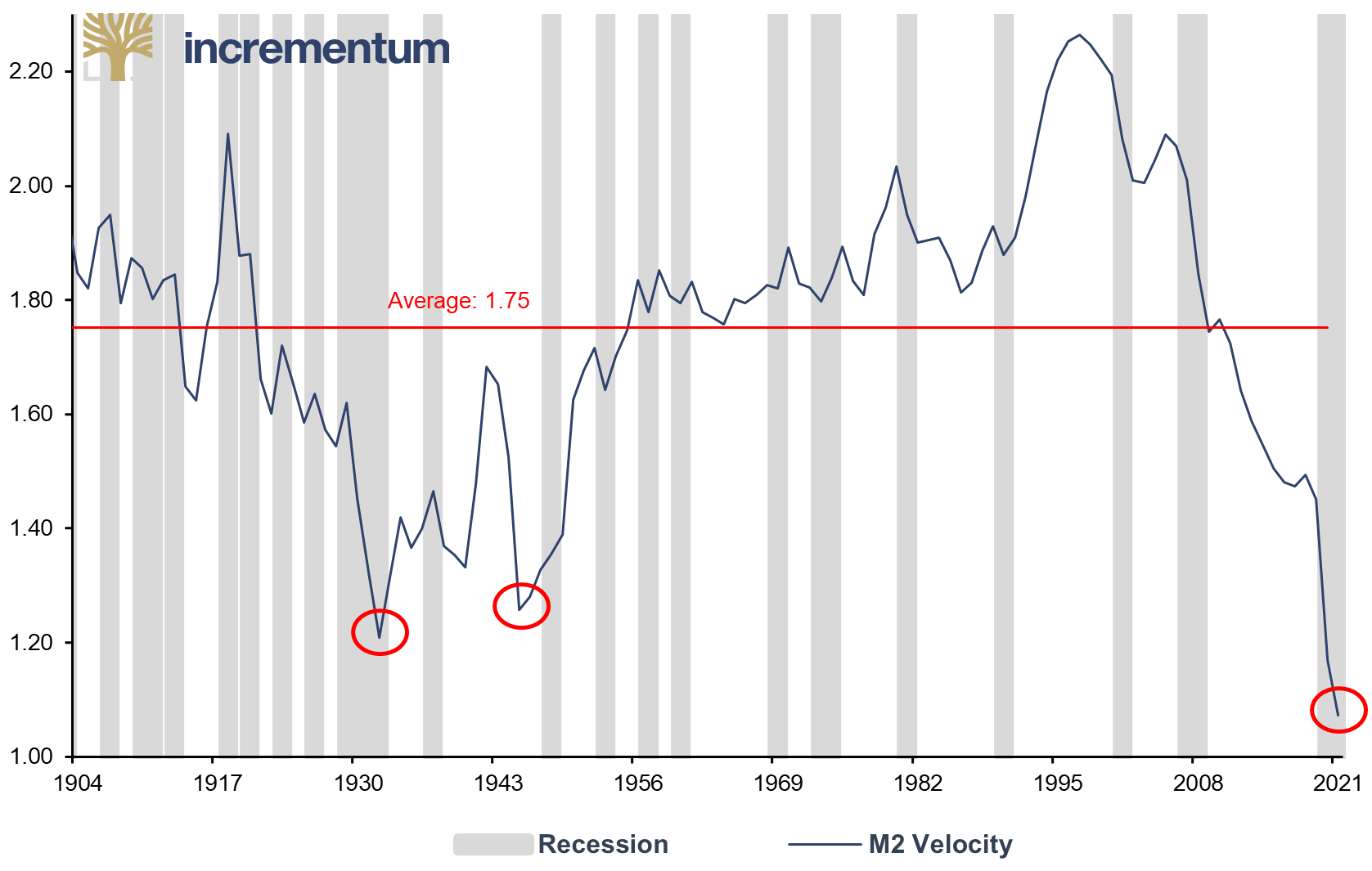

Another point for understanding why inflation will be with us for longer is the development of the velocity of money. As the population’s confidence slowly returns, the velocity of money will normalize, which is why inflation could pick up noticeably. Central banks would have to withdraw liquidity from the system as uncertainty fades and the velocity of money increases. In our opinion, however, their doing so is as likely as a Dutch skier winning the famous Alpine downhill race in Kitzbühel, Austria.

In 1933 and 1946, the velocity of money was similarly low, and in both cases the US government resorted to radical measures. In January 1934, it devalued the US dollar against gold by almost 70%, and in the period 1946–1951 it enforced financial repression in cooperation with the Federal Reserve, which capped interest rates at a low level. Both times, this massive intervention resulted in significantly higher inflation rates in the years that followed. Currently, the velocity of money is at even lower levels than in 1933 or 1946. We expect history to repeat itself and central banks to seek their salvation in financial repression.[14]

M2 Velocity, Q1/1900-Q1/2021

Source: Reuters Eikon, Incrementum AG

The Interest Rate Turnaround and Bitcoin as Swords of Damocles Over the Gold Price?

Many gold investors are surprised that the gold price has been in a consolidation phase since last summer. In our view, one of the key reasons is rising US yields. Classically, the yield curve reflects the expected path of interest rates. In August 2020, the yield curve started to turn at the long end, creating significant headwinds for the gold price. The gold price already appears to be discounting medium-term rate hikes, while eurodollar futures see an 80% chance of a rate hike by December 2022.

Gold (lhs), in USD, and UST10Y (rhs, inverted), in %, 01/2017-05/2021

Source: Reuters Eikon, Incrementum AG

However, a look at the past proves that the gold price can perform strongly even when nominal yields rise, especially when inflation rates rise faster than interest rates. Nevertheless, rising yields pose risks for the gold price in the short term, as long as it is not clear how the inflationary trend will develop. When market participants realize that real interest rates will remain low or even fall further – despite rising nominal yields – the gold bull market should continue.

The fact that rising bond yields trigger nervousness in the markets was confirmed in March, when yields on 10-year US Treasuries rose to 1.75%. As soon as the feel-good zone of inflation is left behind and higher inflation expectations become anchored, major dislocations in the bond markets are inevitable. More and more central banks will be forced to implement a policy of explicit or implicit yield curve control.[15] This would be tantamount to quantitative easing without quantity restrictions. Central banks would have to promise to buy as many government bonds as needed to cap yields.

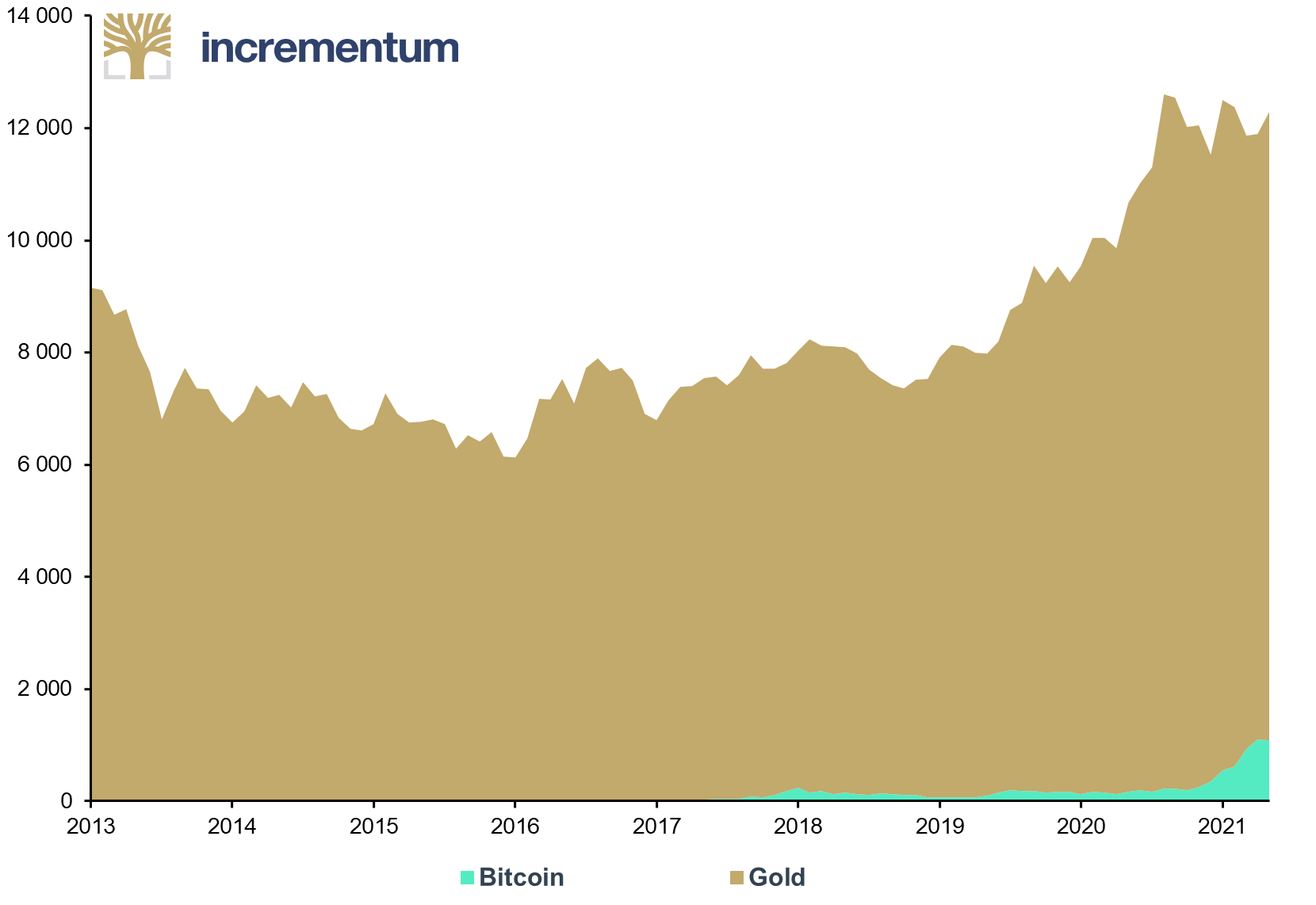

Another explanation for the partly disappointing development of the gold price in recent months is the increasing acceptance of Bitcoin in the traditional financial sector. Indeed, it seems that Bitcoin as a noninflationary store of value is slowly being adopted by institutional investors as well. It stands to reason, therefore, that Bitcoin – and other cryptocurrencies – have absorbed funds that traditionally would have gone into gold investments. In our view, however, this effect has not been decisive for the price development of gold, but neither has it left the gold market entirely unscathed.

Market Capitalization of Gold and Bitcoin, in USD bn, 01/2016-05/2021

Source: Reuters Eikon, World Gold Council, coinmarketcap.com, Incrementum AG

Will digital gold now replace physical gold as an investment? No, it will not. We remain convinced that physical gold will continue to play a fundamental role in asset management in the future, as its portfolio characteristics are unique and the fascination it has always exerted on people remains unbroken. Nevertheless, it makes sense to look at digital stores of value, especially in times when old assets are in danger of being devalued while new assets are being created.

We have been following the Bitcoin phenomenon since 2015 as part of our In Gold We Trust report. In 2019, we made a plea for an admixture of Bitcoin to a gold portfolio in a chapter devoted to that topic.[16] Consistent with that view, we launched an investment strategy as a fund in early 2020, a fund that we are convinced is superior to an individual investment in gold – or in Bitcoin – in many respects. We provide a detailed account of the results of the strategy to date in this In Gold We Trust report.[17]

What’s Next? Yield Curve Control and Financial Repression

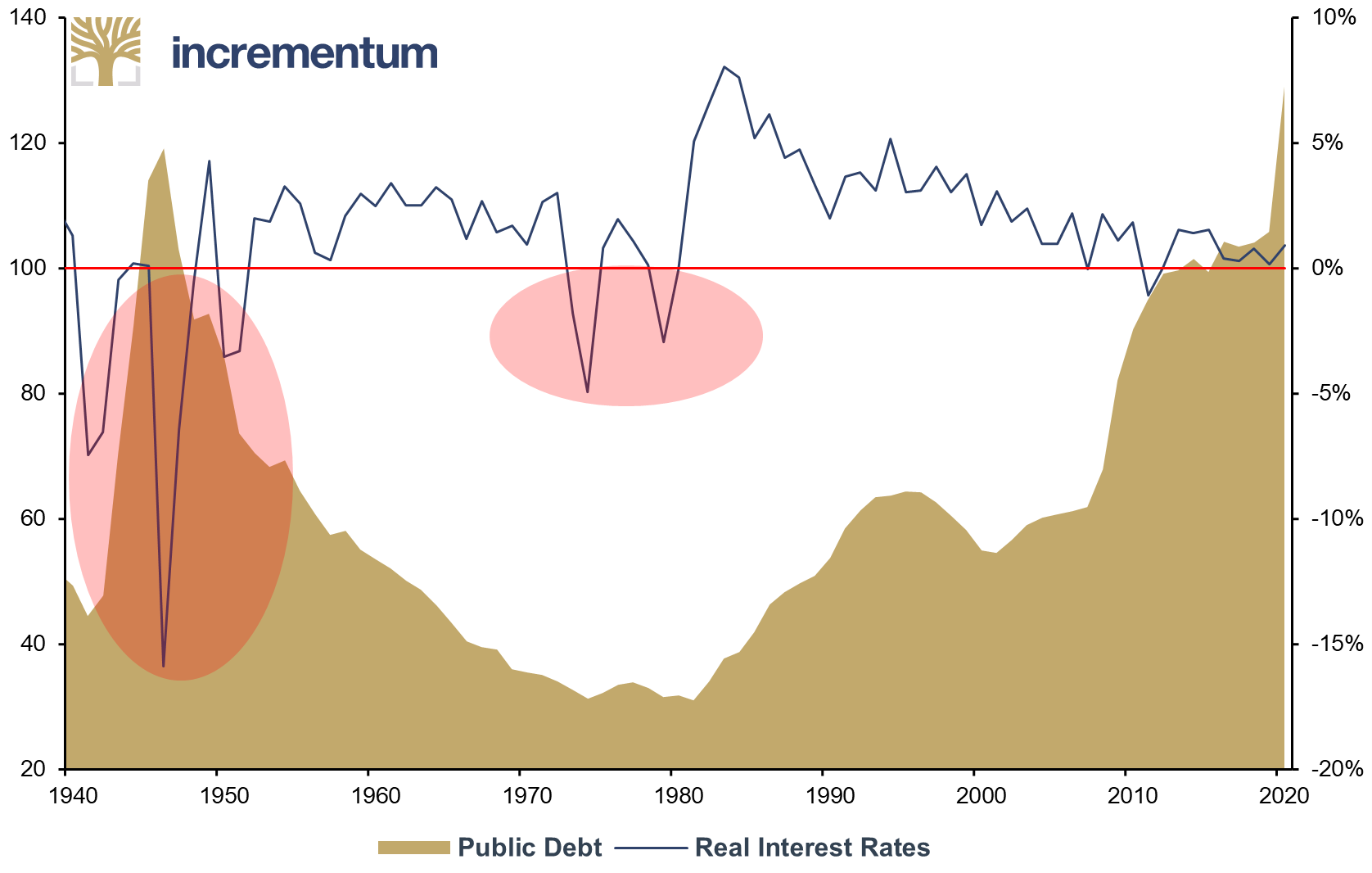

We know this: Public debt in many countries is at its highest level in peacetime. Among the G7 countries, only Canada and Germany have debt ratios of less than 100% of GDP, although even these two countries have significantly higher debt ratios if implicit debt, (e.g., pension entitlements) is added. How will the G7 states be able to overcome this debt situation?

A look at the history books might answer the question. The US ended World War 2 with debt at nearly 120% of GDP, while in the UK it stood at 250%. By the early 1970s, the debt-to-GDP ratio had fallen to about 25% in the US and below 50% in the UK. How was this achieved? The answer: by financial repression, i.e., by capping the yield on government bonds – significantly – below the rate of inflation.

Gross Federal Debt (lhs), in % of GDP, and Real Interest Rates (rhs), 1940-2020

Source: Reuters Eikon, Federal Reserve St. Louis, Nick Laird, goldchartsrus.com, Incrementum AG

After all, the control of the yield curve is by no means new. In 1942, the Federal Reserve made a commitment to the US Treasury to buy enough bonds to cap interest rates at 0.375% for short-term bills and 2.5% for 10-year Treasuries. This significantly mitigated the financing costs of World War 2. This cap remained in place until 1951, with inflation averaging 5.8% per year during this period and as high as 20% in the years immediately following World War 2. As a result, real interest rates were deeply negative and the debt-to-nominal-GDP ratio was able to shrink back to an acceptable level.[18] Conveniently, the Federal Reserve gives itself the legitimacy for future yield curve control:

“The period 1942–47 provides some evidence that the Federal Reserve can lower long-term rates by committing to keeping short-term rates low. The brief period from 1947 to 1948 may also provide additional evidence that long rates can be reduced by direct interventions in the market for long-term Treasuries.” [19]

However, there is one major difference: In 1942, 84% of all Federal Reserve liabilities were backed by gold. At that time, the US owned almost a quarter of the world’s gold. Our friend Daniel Oliver concludes:

“If inflation breaks out and market rate for Treasuries jumps above the Fed’s targets, it will have to purchase the entire stock to control rates. There is no doubt the Fed can do this, but it would herald the final end of the dollar.” [20]

Winners and Losers

A meteorological climate change can have both negative and positive effects on the population, depending on the region and the field of economic activity. Monetary climate change poses risks to investors, but offers also opportunities. Last year, we wrote in this context:

“It is very possible that experimental monetary policy will trigger a renaissance of hard assets. If that thesis is correct, the battered commodity sector should also offer opportunities to courageous contrarian investors.” [21]

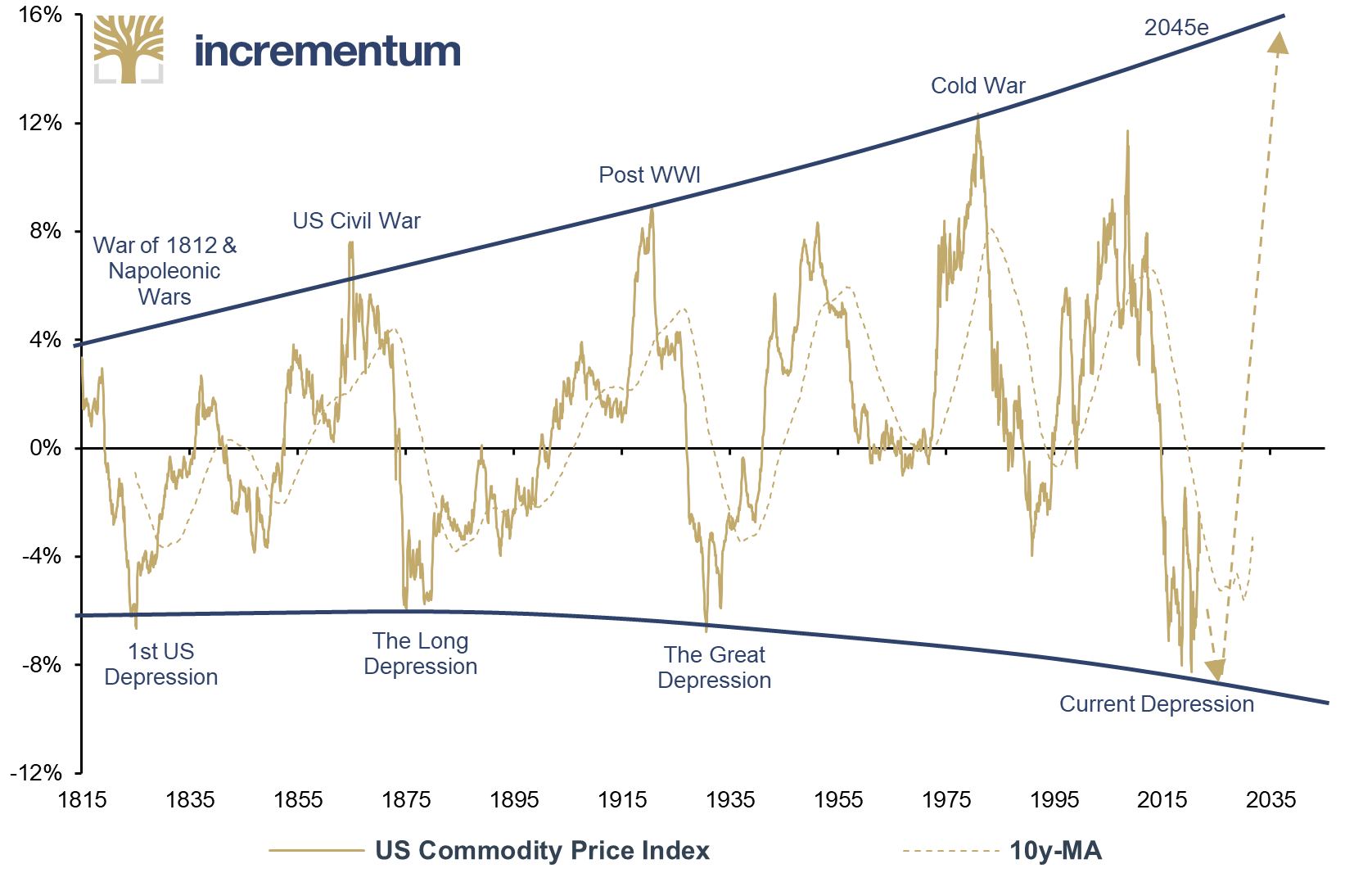

After hibernating for years, commodity prices have now awakened. It is quite possible that the 2010s will turn out to be the 1960s and the 2020s the 1970s. In our view, at any rate, the indications are clearly intensifying that the entire area of inflation-sensitive assets could be at the beginning of a pronounced bull market.

US Commodity Price Index, 10-year rolling CAGR, 1815-2021

Source: Stifel Report, Incrementum AG

As uncomfortable as the dynamics are in general, the conditions for gold could not be better: massively over-indebted economies that will resort to devaluing their currencies as a last resort to reduce their debts. We believe that real interest rates will remain in negative territory for the next decade. In such a market environment, tangible assets, especially commodities, selected equities in the right sector, and obviously precious metals should form the solid basis of the portfolio.

The Golden Decade

The 15th edition of our In Gold We report[22],[23]comes at a time marked by “zozobra”[24], a Spanish term reminiscent of the swaying of a ship in danger of capsizing. This term originated among Mexican intellectuals in the early 20th century to describe the feeling of not having solid ground under one’s feet and feeling out of place in the world. In our opinion, gold has recently proven once again to protect saved assets against these latent uncertainties.

Trust comes from repeatedly fulfilling expectations. In the previous year, gold once again demonstrated its sensitive seventh sense and justified the trust placed in it. It warned the attentive observer that the major weather situation was about to turn.[25] In anticipation and reaction to the fiscal and monetary largesse, gold “delivered” during the calendar year 2020 in US dollars, gaining 24.6%. In euro terms, gold rose by 14.3% and marked new all-time highs in numerous other currencies.

In the wake of monetary climate change, a new approach to debt and the digital printing press is spreading. The probability that this decade will go down in history as an inflationary decade has increased significantly, particularly because the inflationary dynamics already in evidence have proceeded without any significant acceleration in the velocity of money. The potential for a significant rise in inflation in the coming years should not be disregarded.

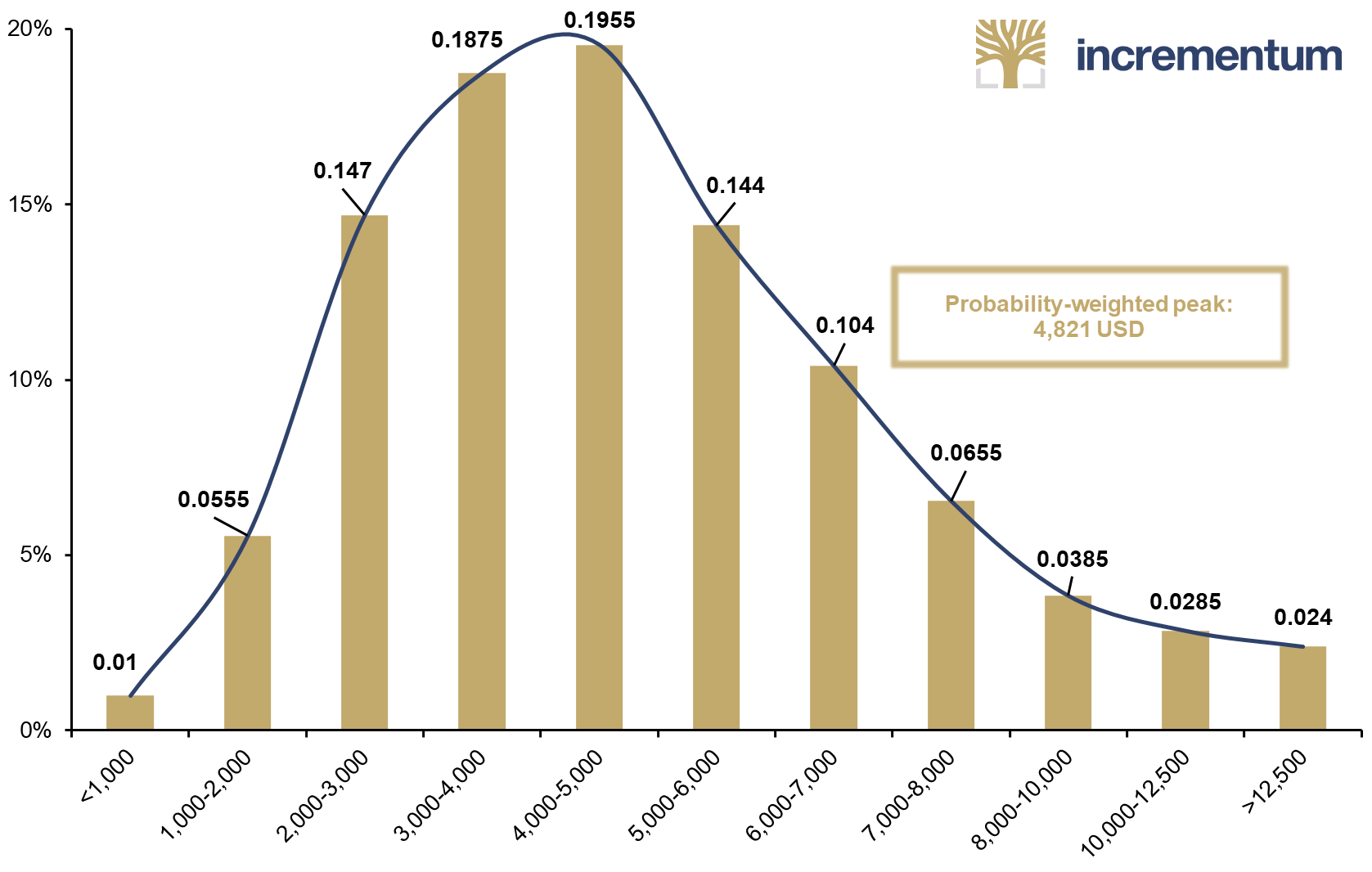

But what does a world with significantly higher inflation rates mean for the gold price? Should inflation rise significantly in the coming years, we believe that five-digit gold prices are conceivable at the end of the decade. Such a scenario would be compatible with further strong increases in Bitcoin prices. Noninflationary assets such as gold, silver, and consumer commodities, but also scarce digital assets are increasingly in demand as stores of value in an environment with clearly negative real interest rates; and the price expressed in paper-money currency is being driven up by a glut of fiat money.

Approximated Gold Price in 2030 by Distribution Probability, in USD

Source: Incrementum AG

We therefore continue to adhere to our last year’s price forecast for the gold price at the end of the decade, based on our proprietary gold price model presented in last year’s In Gold We Trust report. The conservative base scenario, i.e. without any extraordinary inflationary tendencies, results in a price target of USD 4,800 for gold.[26]

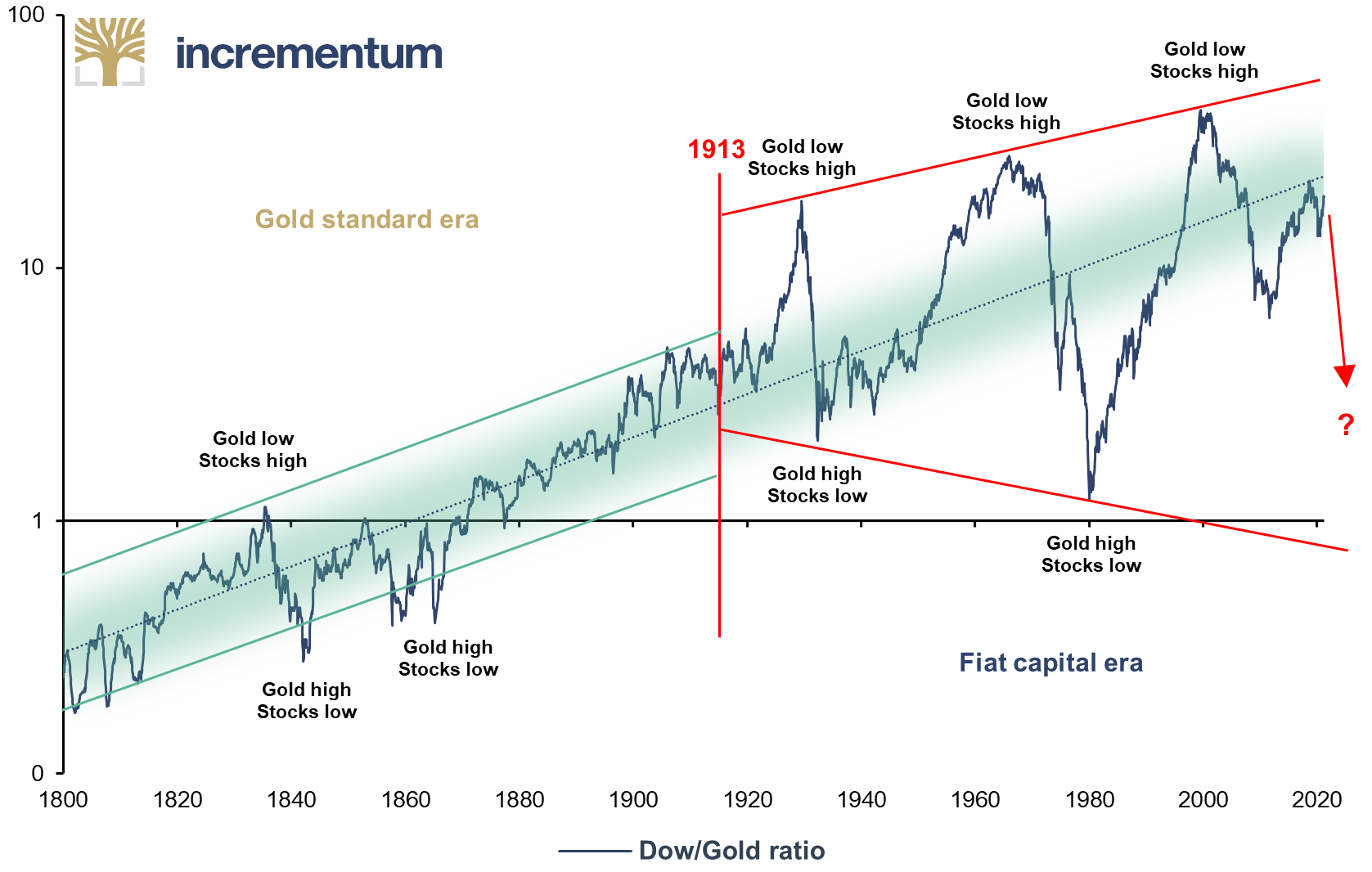

Gold’s price potential is significant not only in absolute terms, but also relative to other asset classes. For example, the Dow/gold ratio, which we pay a lot of attention to, seems to have recently completed its post-Covid-19 rally and could now start resuming its downward trend.

Dow/Gold Ratio (log), 01/1800-04/2021

Source: Nick Laird, goldchartsrus.com, Reuters Eikon, Incrementum AG

Thank you very much!

Year after year, the In Gold We Trust report strives to be the world’s most comprehensive, widely recognized, and enthusiastically perused. Our thanks go first and foremost to our premium partners.[27] Without their support, it would not be possible to make the In Gold We Trust report available free of charge in this form. At the same time, we would like to express our heartfelt thanks to our more than 20 fantastic colleagues for their energetic and tireless efforts!

Studying, understanding, and appreciating the past is critical to preparing for the future. Understanding and preparing for “monetary climate change” is, in our view, the key analytical challenge of the present. That is why this year, in these remarkable but unsettling times, we have again produced a multilayered analysis of gold’s past, present and future. We hope to give you once again, valued reader, a comprehensive, informative and entertaining guide to gold investing.

Now we invite you on our annual tour de force and hope you enjoy reading our 15th In Gold We Trust report as much as we enjoyed writing it.

With warm regards,

Ronald-Peter Stöferle and Mark J. Valek

[1] “Environmental, social, governance” – ESG is used as a broad term for CSR (corporate social responsibility). In other words, the voluntary contribution of business to sustainable development that goes beyond the legal requirements.

[2] Socially responsible investing (SRI), also referred to as social investment, is an investment that is considered socially responsible because of the type of business the company conducts.

[3] See “Gold in the Age of Eroding Trust”, In Gold We Trust report 2019

[4] See “3. Währungen und Werte” (“3. Currencies and Values”), Studienreihe, Donner & Reuschel, February 24, 2021

[5] See Ferber, Michael: “Völlige Enthemmung der Geld- und der Finanzpolitik”, (“Complete Disinhibition of Monetary and Fiscal Policy”), Neue Zürcher Zeitung, December 5, 2020

[6] See “The Dawning of a Golden Decade”, In Gold We Trust report 2020, “Gold in the Age of Eroding Trust”, In Gold We Trust report 2019

[7] See “Central bank digital currencies”, BIS, Committee on Payments and Market Infrastructures, March 2018

[8] See “The rise of Central Bank Digital Currencies”, Kraken Intelligence, April 2021

[9] We recently started offering two fund strategies that invest in both gold and bitcoin. Further information can be found on Incrementum.li.

[10] See Doff, Natasha and Biryukov, Andrey: “Russia Ditches the Dollar in More Than Half of Its Exports”, Bloomberg, April 26, 2021

[11] Saphir, Ann and Marte, Jonnelle: “Fed’s Waller says U.S. economy is ‘ready to rip’”, Reuters, April 16, 2021

[12] Gladwell, Malcom: The Tipping Point: How Little Things Can Make a Big Difference, 2000

[13] See “The Boy Who Cried Wolf: Is An Inflationary Decade Ahead?”, Incrementum, November 30, 2020

[14] See “EMA GARP – Report for the first quarter”, Equity Management Associates, Q1/2021

[15] The Reserve Bank of Australia, for example, has already introduced a YCC. The RBA not only announced its intention to keep the current policy rate stable until 2024 but also committed to a 3-year yield target of 0.10% to keep borrowing costs low for the foreseeable future.

[16] See “Gold and Bitcoin: Stronger Together?”, In Gold We Trust report 2019

[17] See chapter “Bitcoin & Gold – Our Multi-Asset Investment Strategy in Practice” in this In Gold We Trust report.

[18] See “Jurassic Risk and the chomping of the traditional balanced portfolio”, Ruffer Review, March 2, 2021

[19] Carlson, Mark et al.: “2. Federal Reserve Experiences with Very Low Interest Rates: Lessons Learned”, FOMC Memo, December 5, 2008, p. 14

[20] Oliver, Daniel: “The Slingshot”, Myrmikan Research, July 13, 2020, p. 6

[21] “Introduction”, In Gold We Trust report 2020, p. 13

[22] All 14 previous issues of the In Gold We Trust report can be found in our archive at https://ingoldwetrust.report/archive/?lang=en.

[23] This is the abridged version of the In Gold We Trust report 2021. You can download the entire 350 pages of the In Gold We Trust report 2021 free of charge at https://ingoldwetrust.report/download/12773/?lang=en.

[24] See “Feeling disoriented by the election, pandemic and everything else? It’s called ‘zozobra,’ and Mexican philosophers have some advice”, yahoo!news, November 2, 2020

[25] Stoeferle, Ronald: “Gold – The 7th Sense Of Financial Markets”, presentation: Precious Metals Summit, November 11, 2019

[26] See “Quo vadis, aurum?”, In Gold We Trust report 2020

[27] At the end of the In Gold We Trust report you will find an overview of our premium partners, including a brief description of the companies.