A New International Order Emerges

“The world is breaking into two distinct economic zones: the “empire of the sea”, or the “Western block” of nations; and the “empire of the land”, or “Eastern block”. The former’s currency is based on fiat money, and the latter’s on the emerging tandem of commodities, gold and oil.“

Charles Gave

Key Takeaways

- 2022 marks a turning point for the international monetary system as we turn away from the US dollar toward a multi-currency world.

- The freezing of Russia’s currency reserves is comparable to Richard Nixon’s closing of the gold window in 1971.

- While the war distracts the West, Moscow and Beijing are intensifying their cooperation.

- The Petrodollar is reeling: The relationship between Saudi Arabia and the U.S. has rarely been worse, and China is making tremendous progress in the Middle East.

- What the world’s monetary architecture will look like when the dust settles is unclear. What seems certain is that gold and commodities will rise in importance significantly.

The year 2022 will go down as a turning point in the history of international monetary policy. Russia’s attack on Ukraine and the subsequent sanctions have changed everything. The battlefields are not only to be found on the ground in Ukraine; another war is being waged in the financial markets. We could witness the emergence of a new global monetary order in real time. We have been covering many of these issues in the pages of this report since 2017, and now they have entered the mainstream. The idea of a multi-reserve-currency world, no longer dominated solely by the US dollar is gaining a strong foothold. China and Russia are moving closer together, and the oil-rich state of Saudi Arabia, a pillar of US hegemony, is turning its back on Washington – and flirting intensely with Beijing. The West’s sanctions against Russia are stoking the flames. In the words of the Wall Street Journal, “If Russian Currency Reserves Aren’t Really Money, the World Is in for a Shock”.

Europe is once again caught between a rock and a hard place. The role of the euro is more in question than ever. Is it an “instrument of the new European sovereignty”, as former EU Commission chief Jean-Claude Juncker put it? Or is it worthless to the rest of the world because the EU has (so far) gone along with sanctions against Russia? Much in this story is in flux as we write these lines, and many questions remain unanswered. We will therefore take a look at fundamental developments.

At any rate, thanks to its large gold reserves, Europe should at least be well prepared for what is to come. Because what we are seeing here can also be described as the “return of real stuff”, a new monetary world that revolves largely around gold and commodities. It’s something that the Europeans, Russians and Chinese have wanted for many decades, as our timeline will show. Analyst Zoltan Pozsar of Credit Suisse calls this “Bretton Woods III”, but this new system rather deserves a name of its own. Out of the ashes of the gold-backed US dollar and the petrodollar will emerge something completely new, something that no longer has anything to do with Bretton Woods.

The new monetary world order is multipolar – something Jerome Powell confirmed on March 2, 2022, when he said, “It’s possible to have more than one major reserve currency”. Powell also emphasized the advantages of the US dollar in the free struggle of monetary forces: legal certainty and an open, deep capital market. No one, not Europe, not Russia, not China, can match that. At least not for now.

But before we can perceive what a new monetary world would look like, we need to understand the past. We need to go back to 1944, to the founding of the Bretton Woods system, and look at how this system, which is now breaking down, developed. We need to delve into what has been happening since Russia invaded Ukraine; because while the Ukraine war is dominating the headlines, there’s a fight going on in the financial system, and what is happening there points the way to the future.

We will therefore focus on the history of the monetary system as we know it, on the role of gold and the emergence of the euro; the growing friendship between Moscow, Beijing and Riyadh; and Russia’s adventurous plans to create a new, digital world currency.

What Has Happened So Far: The Long History of US Dollar Dominance

To understand how we got into this situation, we need to revisit past decades. It’s not easy to keep track of everything happening, but if there is one theme that keeps coming up, it is this: The use of the US dollar as a reserve currency is a long-term political problem because it gives the US too much power (“exorbitant privilege”), and it’s an economic problem because a national currency is ill-suited as a world currency (the Triffin dilemma).

The solution to both these problems is to use a neutral reserve asset. This can be of natural origin, such as gold or other commodities, or artificially created, such as the IMF’s Special Drawing Rights ts (SDR). Both variants have been considered time and again and attempts have even been made to implement them in rudimentary form – but so far without success.

1940s

Keynes fails at Bretton Woods and the problem takes its course

July 1944: More than 700 delegates from 44 nations meet at the Mount Washington Hotel in Bretton Woods, New Hampshire. Among them: the US, Canada, Australia, Japan, and some European powers. One year before the end of the war, they decide on the world’s new monetary order: the first and, so far, only monetary system based on international treaties.

- The US dollar will be pegged to gold, all other currencies will be pegged to the US dollar. This is a variant of a proposal by the British economist John Maynard Keynes – with one small but important difference: Instead of a new, neutral world reserve currency, yet to be created – called “the bancor” by Keynes – the US dollar will play this crucial role.

- The Bretton Woods Agreement (BW) cements the role of the US dollar as reserve currency and that of US government bonds (Treasuries) as reserve assets. The US dollar is “as good as gold“ and will henceforth play the role of gold in the world monetary system.

- The International Monetary Fund (IMF) and today’s World Bank are created as new, international bureaucracies to prop up the BW system.

1945–1959

After the Second World War, Europe’s economy is at rock bottom. National currency reserves have been depleted. At the same time, there is a high demand for goods from the US, where the industrial base is intact. The result is a large US trade surplus and an acute shortage of US dollars in Europe.

- On paper the IMF and the World Bank are responsible for balancing temporary imbalances by way of loans. But the imbalances are structural, and too large. The US therefore initiates the Marshall Plan to rebuild Western Europe and restore it to solvency.

- The reconstruction of Europe is so successful that the US has its first negative trade balance as early as 1950, a trend that will continue and intensify until today.

- The BW system is now running as planned – but this does not eliminate the systemic problems. In fact, they are just getting started.

- Washington starts to export paper money and import real goods. But the printed paper money is backed by US gold reserves, and those begin to shrink rapidly in the 1950s as other countries exchange their US dollars for gold.

1960s

Triffin discovers his dilemma

In the 1960s, economist Robert Triffin warns of the contradictions in the Bretton Woods system. According to Triffin, the use of a national currency as the main international reserve currency will eventually lead to conflict between said country’s national needs and those of the world economy. Triffin predicts that the gold peg of the US dollar will fail.

- This contradiction was one of the reasons why Keynes had advocated the introduction of a neutral reserve asset at Bretton Woods.

- In response to Triffin, the IMF introduces Special Drawing Rights (SDRs) in 1969. SDRs are a synthetic reserve currency, representing a basket of other currencies.

- Following their introduction, there are many attempts to introduce SDRs as the major international reserve asset and thus replace the US dollar. All attempts fail due to US resistance.

As early as the 1960s, several measures are taken to stabilize the BW system. The main concern is to maintain the fixed gold price ratio of USD 35 per ounce. Anything else would amount to a devaluation of the US dollar.

- To this end, the London Gold Pool is created in November 1961 and charged with manipulating the free gold market in order to depress the price.

- Under the BW system, it is not possible for individuals to exchange US dollars for gold. Private ownership of gold has even been forbidden to US citizens, since 1933.[1] Only foreign governments and central banks have the possibility to exchange their US dollars for gold.

In Europe, resentment against the Bretton Woods system grows from the 1960s onward. People feel trapped in an unfair system in which Europe’s citizens have to subsidize the high standard of living in the United States.

- The French, under former General Charles De Gaulle, are particularly critical of the BW system. France is the nation that most actively exchanges US dollars for gold.

- French Finance Minister Valéry Giscard d’Estaing coins the term exorbitant privilege to describe the ability of the US to print money almost at will and receive real goods in return.

- In 1965, De Gaulle warns of a US dollar crisis in a televised speech and makes the case for a return to the gold standard. His words are strongly reminiscent of the criticisms of Keynes and Triffin. De Gaulle maintains that the US dollar cannot be a “neutral and international medium of trade” and is in fact “a credit instrument reserved for only one state”.

In March 1967, the then president of the Deutsche Bundesbank, Karl Blessing, sends a letter to the board of the Federal Reserve. Blessing promises that Germany will not imitate the French and that Bonn will refrain from exchanging its US dollar reserves for gold in the interest of international cooperation. The so-called “Blessing letter” of March 30, 1967, goes down in history.

- A few years later, in May 1971, Karl Blessing describes the concession as a mistake: “I declare to you today that I myself feel personally guilty in this area. I should have been more rigorous with America at the time. The dollars that accrued to us should simply have been rigorously exchanged for gold.”

- In this interview, Blessing also outlines what the euro should eventually be: a European central bank, independent of the nation states, with clear rules and a hard currency: “There is no doubt that, if we really had the political will in the EEC, we could form a hard currency bloc whose rates could then fluctuate against the dollar. That would have taken us away from the US dollar standard, which we have today. After all, we practically have the dollar standard.”

- At the end of 1970, the “Werner Report”, named after Pierre Werner, Prime Minister of Luxembourg, is published. It is the first real plan on the part of Europe to create an economic union within a decade and is regarded as the starting signal for efforts to create a common currency.

1970s

In early August 1971, France under De Gaulle sends a warship to New York to pick up physical gold that France was to receive in return for its US dollars.

The Nixon shock and the birth of the petrodollar

On August 15, 1971, US President Richard Nixon ends the Bretton Woods monetary system after a quarter-century. He cancels the gold peg of the US dollar. At first, this is merely “temporary” and is intended to “strengthen” the US economy. At this point, the US has “only” about 8,000 tonnes of gold in its reserves.

- Europeans are shocked at the unilateral decision. Instead of giving up the “exorbitant privilege” and moving the world to a neutral reserve asset, the US continues to expand its privilege. Starting in 1971, Washington no longer has to fear losing gold when printing money.

- The 1970s see high inflation rates and two oil shocks. The production of US oil reaches its temporary peak at the end of the 1960s, and the Arab oil countries see Nixon’s move as a devaluation of the US dollar. Prices rise and crises break out in the Arab region. For the first time, Western industrialized countries have to deal with oil shortages.

- In 1972, US President Richard Nixon visits communist China, marking a turning point in relations between the two countries. Nixon spends seven days in China. This signals the start of a new form of cooperation that will jumpstart China’s economic development.

In July 1974, newly appointed US Treasury Secretary William Simon flies to Saudi Arabia. The first oil crisis has hit the United States. Simon has previously served as Nixon’s energy expert and before that headed Treasury trading at Salomon Brothers. He is a proven expert on the oil and bond markets.

- At these meetings, a deal is negotiated that is to have a massive impact for decades to come. In return for military and political support, Saudi Arabia agrees to recycle its petrodollars into US Treasuries.

- The petrodollar is born. From this point on, the world’s reserve currency, the US dollar, is no longer backed by gold but by “black gold”. From then on, all countries must hold large reserves of the US currency to pay their energy bills.

The end of the 1970s and the Volcker shock

In 1976, the Bretton Woods system is formally buried by the Jamaica Accords. In the early 1980s, all developed countries allow their currencies to fluctuate. For the first time in history, the whole world is on a pure paper money standard, with one exception: Switzerland formally keeps the franc pegged to gold until 1999.

- In 1979, the US dollar is under tremendous pressure due to the persistently high inflation of recent years. In August of that year, Paul Volcker takes over as head of the Federal Reserve.

- In March 1979, the European Monetary System is created. For the first time, all exchange rates of the participating countries are linked to each other by means of the European currency unit (ECU). This later becomes the euro.

- That summer, core inflation in the US reaches 12%. The gold, silver and commodity markets react sensitively and prices shoot up, which makes the Federal Reserve under Volcker nervous.

- In October 1979, politicians and central bankers of the West meet at an IMF gathering in Belgrade. In the United States, the White House has long since declared the fight against inflation a “national priority”. In Belgrade, Paul Volcker seeks the advice of the Europeans, consulting with German Chancellor Helmut Schmidt and Bundesbank Chairman Otmar Emminger, among others.

“In Belgrade … it became obvious to Volcker that a collapse of the US dollar was a very real possibility, perhaps leading to a financial crisis and pressure to remonetize gold, which the United States had fought doggedly for over a decade. To forestall this, there was only one possible course of action: do whatever was necessary to strengthen the dollar.” [2]

Volcker cuts his trip abroad short and returns to Washington prematurely on October 2: “With his ears still resonating with strongly stated European recommendations for stern action to stem severe dollar weakness on exchange markets.”

- He organizes a secret Federal Reserve meeting on Saturday, October 6, 1979.

- Volcker prevails, setting the stage for a general change of course within the Federal Reserve. Controlling money supply growth should be the most important tool in the fight against inflation in the future. The reserve requirements for banks are tightened.

- In 1979, annual inflation in the US rises to 14%. In the following year, the gold price was to peak at around USD 850. At the beginning of 1981, short-term interest rates would peak at around 20%. Volcker would succeed in stopping inflation – at the expense of the US economy, which slides into recession.

1980s

The stability of the 1980s

In the 1980s, the system stabilized. The Europeans, however, have by now long been working on their own currency, which should make them independent of the US dollar system. The advocates of the SDRs and the IMF were not idle either. In 1984, economist Richard Cooper proposes a global single currency – with a common monetary policy and a common central bank. The US, Europe and Japan are to be the first nations to join.

Photo credit: www.coverbrowser.com

“Get ready for a world currency” – This was the headline of “The Economist“ on January 9, 1988. In the article, the creation of a global monetary union is suggested. In this vision the IMF is to assume the role of the world central bank and its SDRs the role of the world currency. In the description, it is striking that the envisaged construction strongly resembles that of the later Euro area: A system whose rules must be followed by all participating states. The Economist calls the new currency phoenix and predicts its introduction by 2018.

“Each country could use taxes and public spending to offset temporary falls in demand, but it would have to borrow rather than print money to finance its budget deficit. With no recourse to the inflation tax, governments and their creditors would be forced to judge their borrowing and lending plans more carefully than they do today.”

1990s

The introduction of the euro

In December 1995, the EU states agree on a name for the common currency: the euro. On January 1, 1999, the euro is introduced. Gold plays an important role for the new currency from the very beginning. But under the first ECB president, Wim Duisenberg, the euro is not pegged to gold as the US dollar was under the Bretton Woods system.

Instead, gold is treated anew on the Eurosystem’s balance sheet as an independent asset, separate from the currency. Gold is listed on the first line on the ECB’s balance sheet. Four times a year, the value of the reserves is adjusted to the market value. This turns the monetary world upside down.

- A rising gold price is good for the euro because it strengthens the balance sheet. At the same time, it is a signal to EU citizens, who have free access to physical gold, that if the central bank’s management doesn’t suit them, they can save in hard, neutral “money”: gold.

- This system of market valuation of gold has now also been adopted by the central banks of Russia and China, but not by the US.

- To safeguard this system, the purchase and sale of “investment gold“ is exempted from VAT throughout the EU in October 1998.

- On September 26, 1999, a group of European central banks sign the first Central Bank Gold Agreement (CBGA). The aim: to reassure the market that they will curb their gold sales in the future. The gold price finds its bottom in the coming years and eventually starts to rise.

- Because the UK is still selling about 400 tonnes of gold at rock-bottom prices after the CBGA is signed under then-Chancellor of the Exchequer Gordon Brown, the period between 1999 and 2002 is today nicknamed the “Brown Bottom”.

2000s

The fact that the euro is also intended as an energy and reserve currency from the very beginning is never concealed by EU politicians. Even before the introduction of euro cash on January 1, 2002, the new currency is causing a stir. In November 2000, Iraq’s President Saddam Hussein decides to switch from using US dollars to euros in the oil trade. The US protests loudly and warns Hussein against this step.

- In February 2003, it is clear: Iraq has made an economically good decision by switching to the euro; the warnings from the US were all wrong. The euro exchange rate has risen significantly over the past three years, and interest rates are also higher than on US dollar accounts.

- In March 2003, the US attacks Iraq. Saddam Hussein is overthrown, and the oil trade is switched back to US dollars. Germany and France are among the biggest opponents of the invasion and refuse to support the US.

The financial crisis and its consequences

In the wake of the great financial crisis and the Lehman bankruptcy, concerns grow again that the US dollar system may have reached its end.

In March 2009, the head of the People’s Bank of China (PBoC), Zhou Xiaochuan, speaks out for the first time. In a remarkable speech at the Bank for International Settlements (BIS), he calls for a move away from the US dollar and the establishment of a new monetary system. China’s central bank chief makes direct reference to the entire monetary history since 1944 and quotes Keynes and his bancor idea.

In November 2009, legendary journalist Robert Fisk reports on an agreement among China, Russia, Japan, the Arab world, and France (i.e., the euro area) to move away from the US dollar-based system.

“In the most profound financial change in recent Middle East history, Gulf Arabs are planning – along with China, Russia, Japan and France – to end dollar dealings for oil, moving instead to a basket of currencies including the Japanese yen and Chinese yuan, the euro, gold and a new, unified currency planned for nations in the Gulf Cooperation Council, including Saudi Arabia, Abu Dhabi, Kuwait and Qatar. ‘These plans will change the face of international financial transactions,’ one Chinese banker said. America and Britain must be very worried. You will know how worried by the thunder of denials this news will generate.”

2010s

In November 2010, Vladimir Putin says that Russia will one day join the euro or form a monetary union with Europe.

Also in November 2010, World Bank President Robert Zoellick advocates gold as the “reference point“ for a new monetary order.

In February 2011, then IMF chief Dominique Strauss Kahn proposes replacing the US dollar as the world reserve currency with SDRs. He is arrested in New York in May 2011 and resigns as IMF head. The charges against him are dropped by the public prosecutor’s office after several months.

The PBoC announces in November 2013 that it is no longer in China’s interest to expand its reserves of US government bonds.

On July 5, 2014, the then-CEO of the European oil company Total, Christophe de Margerie, speaks out in favor of using the euro in oil trading. On October 21, 2014, de Margerie dies in an accident at Moscow airport. The Total CEO was on his way back from a meeting with Russian Prime Minister Dmitry Medvedev. De Margerie was considered a friend of Russia and a critic of the sanctions imposed on Russia by the West at the time, because of the annexation of Crimea. His private jet had collided with a snowplow. An investigation concludes that the driver of the snowplow was drunk.

Russia and China sign a gas deal in May 2014 that is described as the “holy grail”. It is negotiated for 10 years and is to extend over 30 years.

September 2014: China launches an international gold board in Shanghai, denominating the price of gold in yuan to increase international participation in the Chinese gold market.

Luxembourg central banker and ECB director Yves Mersch says in November 2014 that the ECB “could buy gold to stimulate the economy”. It is the clearest signal yet that euro area central banks are no longer on the sell side of gold.

In his last major speech as EU Commission chief at the end of 2018, Jean-Claude Juncker directly addresses the international role of the euro, saying it needs to be strengthened and calling EU energy trading in US dollars “absurd”. His speech is entitled “The Hour of European Sovereignty”.

2020s

From 2018 to 2022, many bilateral steps will occur between countries such as China, Russia, Iran, Saudi Arabia, and the Europeans. Trade is often switched to national currencies. But one thing never happens: another global currency conference.

Instead, the monetary system is redone by political action – such as the freezing of Russian US dollar and euro currency reserves following Russia’s attack on Ukraine in spring 2022.

When money is weaponized

The West’s freezing of Russian gold and foreign exchange reserves marks the biggest upheaval in the international monetary system since the Nixon shock of 1971 and the subsequent shift from a US dollar-based gold-forex standard to a system of flexible exchange rates with the unfunded fiat US dollar as the anchor.

“This is a major break in the international monetary order created by Bretton Woods II. The sanctions create de facto a new order in which central bank reserves are now worth only as much as the dominant reserve currencies issuing them want them to be.”

A country’s currency reserves serve as its piggy bank for difficult times. Russia has played a special role in the process of de-dollarization long before the war in Ukraine. Among the world’s powerful, Vladimir Putin has always been the one who has most clearly opposed the supremacy of the US dollar. In particular, the fact that the US uses the world currency as a tool for sanctions has always been a thorn in his side. Thus, Putin said in 2019: “The United States started using dollar settlements as a tool in the political struggle for some purpose, imposing restrictions on dollar use and cutting the branch they are sitting on, but they will fall with a crash soon”.

In the summer of 2021, Putin had another warning ready for Washington, a warning based on his own experience with the fall of the Soviet Union: “The problem with empires is that they think they can afford small errors and mistakes…. There comes a time when they can no longer be dealt with. And the US … is walking straight along the path of the Soviet Union”.

Clear words, which, however, did not land on open ears. Following Putin’s attack on Ukraine, the monetary system has become a theater of war. The Financial Times also writes about the West’s sanctions against Moscow:

“The plan agreed by Yellen and Draghi to freeze a large part of Moscow’s $643bn of foreign currency reserves was something very different: they were effectively declaring financial war on Russia…. This is a very new kind of war – the weaponization of the US dollar and other Western currencies to punish their adversaries.”

In recent years, Russia has massively shifted its reserves from US dollars to euros. The Russian Central Bank now holds only about 7% of its reserves in US dollars. The fact that Moscow concluded a major gas deal with Beijing in euros, just a few weeks before the invasion, is also an indication that Putin did not expect his euro reserves to be sanctioned. After all, it has long been a goal of the EU to use the euro to make itself independent of the dominance of the US dollar.

That is a goal that now seems far away, as Europe has clearly sided with Washington on the Russia issue – at least so far.

The Western sanctions affect around two-thirds of Russia’s currency reserves. The reserves have not disappeared, but Moscow currently has no access. Importantly, the sanctions do not affect the flow of US dollars and euros to Russia at this time. The EU has also not yet imposed an energy embargo. Instead, a complicated construct has been agreed upon in which EU states deposit euros into an account at Gazprombank, euros that Russia then converts to rubles.

Still, the sanctioning of reserves is a huge step with huge consequences. The West has “closed the FX window”, in the words of our friend Luke Gromen – who is referring directly to the closing of the gold window by US President Richard Nixon in 1971. Well-known economist Kenneth Rogoff takes a similar view:

“It’s an absolutely radical measure to try to freeze assets at a major central bank. It’s a break-the-glass moment…. If you want to look at the long-run picture of dollar dominance in the global economy, believe me, China’s looking at this. They have, I don’t know, $3 trillion in dollar reserves.”

And China is not the only country where a rethink is now taking place. Louis-Vincent Gave puts himself in the head of rich Saudis:

“Is it too much of a stretch to imagine Western governments in a few years’ time deciding that fossil fuel producers must pay for climate-change-induced damage, leading to Saudi royals facing asset confiscation? To be clear, I am not saying this will happen. Yet if I was a Saudi prince, a few weeks ago I would not have worried about having my Swiss bank account closed; today I would be hedging myself. Previously, such wealthy investors could own assets in the US or Western Europe in the knowledge that while returns on capital may be lousy, at least the return of that capital was assured. If such certitude no longer exists, what is the point of earning US dollars or euros?”

Like Russia, Saudi Arabia is an oil state with an authoritarian ruling structure. As we will show later, their relations with the US are in tatters. It can therefore be assumed that the royal family in Riyadh is following all sanction steps very closely.

Here are Russian President Vladimir Putin’s clear words on sanctions:

“The illegitimate freezing of some of the currency reserves of the Bank of Russia marks the end of the reliability of so-called first-class assets. In fact, the US and the EU have defaulted on their obligations to Russia…. Now everybody knows that financial reserves can simply be stolen. And many countries in the immediate future may begin – I am sure this is what will happen – to convert their paper and digital assets into real reserves of raw materials, land, food, gold.”

This is a strategy that China, for example, has been implementing for a long time. The Middle Kingdom is sitting on large quantities of industrial and agricultural raw materials. For many years, they have been buying up land, assets and raw material deposits all over the world. The Greek port of Piraeus is only the most famous example. Putin may talk about the future, but he knows full well that the development described has long since begun.

Now, we have certainly pointed out more than once in the past that gold has no counterparty risk as long as you keep it yourself – and in physical form. Our friend Douglas Pollitt comments on this as follows:

“Who knew credit-based money was so easy to take? But of course it is – by its very nature credit requires a counterparty and if that counterparty chooses not to honor your credit, well, that’s about that. By contrast gold is a ‘credit’ with no one on the other side to rug-pull you.”

The repatriation of gold reserves of the Germans, Austrians and Dutch in 2015 to 2018 suddenly appear in a completely different light. Russia holds around 20% of its reserves in gold and that gold is located exclusively in Russia. Moscow has also made no moves to sell this gold so far. Nevertheless, the West is trying to block this part of the reserves as well and is banning trade in Russian gold everywhere possible: in the countries of the G7 and the EU. Admittedly, no one can really prevent Russia from using gold as currency in trade with, say, China, India, or other countries that do not want to comply with Western sanctions.

At the beginning of the crisis it was speculated that Russia might be forced to sell their gold. They decided to take a different path.

Putin’s golden move

Much has been written about Vladimir Putin’s gold plans. Russia has been increasing its gold reserves for years – not without reason. But no one really expected Putin’s next move. Instead of selling gold, the Kremlin set a fixed buying rate for gold at the end of March: 5,000 rubles for a gram of gold. At the same time, they announced that they would only accept rubles for gas deliveries (and later for other commodities).

The combination of these two steps led to a de facto link between gas and gold, which was intended to stabilize and appreciate the ruble. It worked. And it worked so well that the Russian Central Bank lifted the fixed price on April 8. It did not, however, stop buying gold per se, but said it would “negotiate” prices in the future.

Three days after the central bank announced it would buy gold from local banks and producers for rubles, Putin’s gas-for-rubles policy came into play. Here, the impact of Western sanctions is directly observable. Russia has no interest in receiving US dollars or euros when they can be frozen immediately. Russian companies are now also required by law to exchange at least 80 percent of the foreign currency they receive into rubles. Putin’s announcement reads as follows:

“I would like to stress once again that in a situation where the financial system of Western countries is used as a weapon, when companies from these states refuse to fulfill contracts with Russian banks, enterprises, individuals, when assets in dollars and euros are frozen, it makes no sense to use the currencies of these countries.

In fact, what’s going on, what’s already happened? We supplied European consumers with our resources, in this case gas, and they received it, paid us in euros, which they then froze themselves. In this regard, there is every reason to believe that we have supplied part of the gas supplied to Europe virtually free of charge.”

At the beginning of April, Kremlin spokesman Dmitry Peskov spoke out. He said that the gas-ruble deal was only the “prototype“ and that the model would soon be extended to other export goods. He called the blocking of Russian currency reserves by the West a “robbery”.

What are the long-term goals of this policy? Peskov leaves no doubt about it: The Kremlin wants a new world monetary system to finally replace the last remnants of Bretton Woods: “It is obvious – even if this is currently a distant prospect – that we will come to some new system, different from the Bretton Woods system”.

What followed Putin’s announcement was European political theater. The EU countries understandably could not accept suddenly switching to rubles. And while much of the debate in the media revolved around an oil and gas embargo against Russia, German Chancellor Olaf Scholz had to ask Putin to at least continue to accept euros. Putin relented, but not completely.

Europe may continue to pay in euros, Putin said, but the money must flow into a specific account at Gazprombank. This is conveniently exempt from the sanctions, a circumstance that the new deal cements. Since the beginning of April, the gas trade between Europe and Russia has looked like this: Russia allows the gas to continue flowing in exchange for euros or US dollars paid to Gazprombank. The bank then exchanges the money for rubles – the euros concerned are exempt from the sanctions. However, the debt is not discharged until the ruble amount is credited to the seller’s account.

That way, both sides can save face. German Chancellor Olaf Scholz and the other EU heads of government can claim that they will continue to insist on payment in euros. Putin can say that he will exchange the money for rubles immediately. And despite the official hostility, both sides are de facto working to change the currency system and end US dollar dominance – a goal Europe and Russia have shared for many decades.

Today, Russia basically does not care in which currency payment is made – as long as this currency is convertible into gold and/or rubles. After the deal with Scholz, this is only not the case for the US dollar: Russia has now opened up the energy market for all other currencies. This is a big step.

No one has explained it better than Pavel Zavalny, a Russian politician and chairman of the Duma’s energy committee. “Hard money,” he said recently, “is only gold for Russia. Friendly nations (and Europe) may also pay in national currencies”. Only one currency is not accepted, Zavalny said: “The dollar ceases to be a means of payment for us, it has lost all interest for us.” And Zavalny added that from the Russians’ point of view, the US dollar is worth no more than “candy wrappers.”

In this interview, Zavalny even showed a willingness to accept Bitcoin for gas, a detail that was heavily emphasized in global coverage of the story. One gets the impression, however, that the Russians were primarily concerned with one central point. Something along the lines of: If that’s what our friends want, they can pay however they want, even in Bitcoin. However, states classified as hostile, such as the EU states and the US, will only be able to pay in rubles or gold.

Zoltan Pozsar’s vision: Bretton Woods 3.0

No one in the financial and mainstream media has taken a closer look at these developments than Zoltan Pozsar, an analyst at Credit Suisse. Similar to our friend Luke Gromen, who speaks of the “closing of the FX window,” Pozsar also sees the freezing of Russian currency reserves as a rupture in the international currency system. After Bretton Woods, i.e., the US dollar-gold peg from 1944, and Bretton Woods 2, i.e., the petrodollar/eurodollar standard from 1971, he sees Bretton-Woods III dawning with the war of 2022. Bretton Woods III, Pozsar says, will be dominated by more nationalism and protectionism, by higher military budgets and a much greater focus on real assets like gold or commodities, and by inflation – at least in the West: “This crisis is not like anything we have seen since President Nixon took the US dollar off gold in 1971 – the end of the era of commodity-based money.” And Pozsar continues: “When this crisis (and war) is over, the US dollar should be much weaker and, on the flipside, the renminbi much stronger, backed by a basket of commodities.” Finally, he sums up, “After this war is over, ‘money’ will never be the same again.”

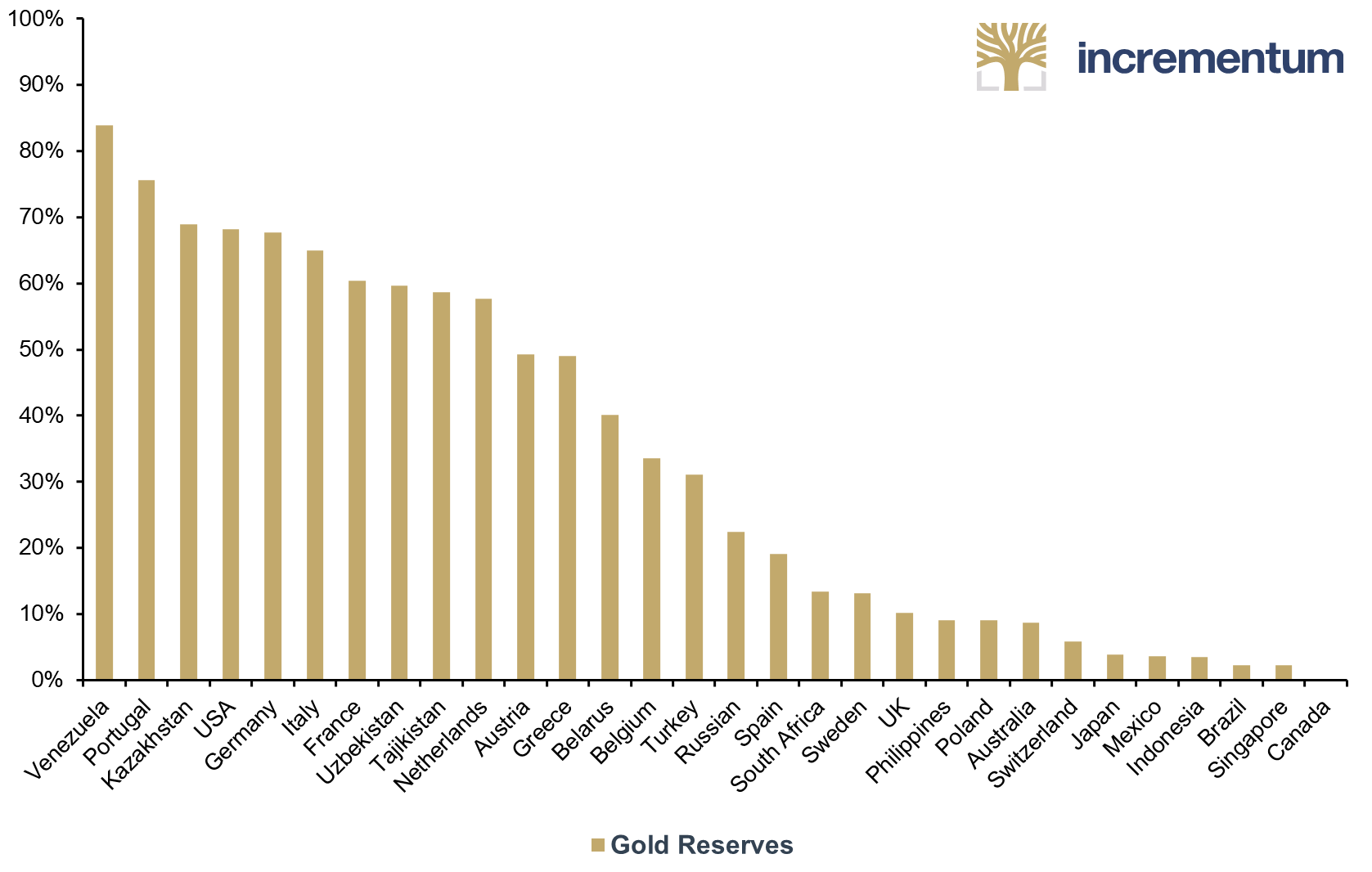

What is striking in view of the sanctions and this new phase of realpolitik is that Western Europe seems to be in a good position – especially when it comes to gold. With more than 12,000 tonnes, the euro area holds the largest gold reserves in the world. The US still has around 8,000 tonnes. And if you look at the importance of gold reserves relative to other currency reserves, the picture is also clear.

Countries such as Germany (66%), Italy (63%) and France (58%) are well prepared for a world in which commodities act as currency anchors, even if they can hardly boast any domestic commodity production themselves. Portugal, the Netherlands and Austria are also betting on gold, along with the “Stan“ states: Kazakhstan, Uzbekistan and Tajikistan.

Gold Reserves, in % of Total Reserves, Q1/2022

Source: World Gold Council, Incrementum AG

Russia and China are building an alliance – and a new world currency

The fact that the Eurasian Economic Union (EAEU) is working together with China on a “new global monetary system” would have been a sensation a year ago. Even more so, since none other than the influential economist and politician Sergey Glazyev is pushing this plan. Today, after the collapse of cooperation between the West and the East, news of a new monetary system is hardly surprising. But it is relevant nonetheless, as these plans also reveal much about the growing cooperation between Moscow and Beijing. They also fit Zoltan Pozsar’s vision of the monetary future.

On March 11, a videoconference of representatives of China and the Eurasian Economic Union (read: Russia) agreed to plan an “independent international monetary and financial system”.

“As a result of the discussion, it was decided to develop a project for an independent international monetary and financial system. It is assumed that it will be based on a new international currency, which will be calculated as an index of the national currencies of the participating countries and commodity prices.”

In an interview with the Russia-friendly journalist Pepe Escobar, Sergey Glazyev elaborates on how he envisions this financial and monetary system of the future. He outlines the formation of an Eastern IMF that would operate completely independently of the current system. At its core is to be a new, synthetic currency backed by both national currencies and commodities. This resembles a practical implementation of the system outlined by Zoltan Pozsar on the basis of purely economic considerations.

Glazyev expects the “imminent disintegration” of the US dollar-based global financial system, which will rob the US of its power base. This would be the final step in a development that has been underway for 30 years. In Glazyev’s timeline, this transition to a new global economic order already began with the end of the Soviet Union. The US hegemony in the monetary system will be replaced by a combination of the systems that have been established in China and India in recent decades. Glazyev speaks of a “combination of the advantages of centralized planning and a market economy.”

Glazyev describes three phases of the transition. In phase one, many nations would revert to their own currencies in international trade. This is a trend that we have not only seen since the war in Ukraine.

“This phase is almost over: after Russia’s reserves in dollars, euro, pound, and yen were ‘frozen’, it is unlikely that any sovereign country will continue accumulating reserves in these currencies. Their immediate replacement is national currencies and gold.”

The second step is to create pricing mechanisms that do not require the use of the US dollar. This is also a development we have been seeing for some years, for example in China, where gold and oil are now priced in yuan. But the yuan will not become the direct successor to the US dollar, says Glazyev, because it is not convertible and Chinese capital markets are partly closed to outsiders.

Gold could not take on this role, either, as it is too impractical as a means of payment. Therefore, something new is needed: a “new digital payment currency”. This is the third step:

“The third and the final stage on the new economic order transition will involve the creation of a new digital payment currency founded through an international agreement based on principles of transparency, fairness, goodwill, and efficiency. I expect that the model of such a monetary unit that we developed will play its role at this stage. A currency like this can be issued by a pool of currency reserves of BRICS countries, which all interested countries will be able to join.”

At first glance, the plan resembles that of the West, based on the Special Drawing Rights that were created in the 1960s as a neutral reserve asset, based on a currency basket. With one difference: The currency basket of the East will also include a “price index“ of important commodities, according to the Russian economist and politician: gold, industrial metals, oil & gas, grain, sugar – and even water.

Every country in the world should be able to participate in the new system. At the same time, debts accrued in the old system could be declared null and void if one wanted to – a process that Glazyev already observes and that poses a further threat to the US dollar system.

It is important to note, however, that this plan is probably not currently being implemented in the way Glazyev envisions. He sees the Russian Central Bank as still being under the influence of the West. It will take time for Russia’s blocking of US dollar reserves to convince other countries that a new system is needed, Glazyev says.

But he is not fighting alone. In an interview at the end of April, for example, the powerful former intelligence chief, Nikolai Patrushev, reported that a group of experts was already working on covering the ruble with gold and raw materials. In doing so, Patrushev, a close ally of Vladimir Putin, provides insight into Russia’s specific plans. To create an independent monetary system, there must be a way to anchor the value of the currency – without “tying” it to the US dollar, Patrushev says.

This point is important, because it is not just about power games and the conflict between West and East, but about basic economics. To truly break away from the US dollar, a new reference point is needed, i.e. gold and commodities, because Russia’s true wealth is stored in oil and gas. Patrushev comments on this as follows:

“The West has unilaterally appropriated an intellectual monopoly on the optimal structure of society and has been using it for decades…. We are not opposed to a market economy and participation in global production chains, but we are clearly aware that the West allows other countries to be its partner only when it is profitable for itself. Therefore, the most important condition for ensuring Russia’s economic security is to rely on the country’s internal potential, a structural adjustment of the national economy on a modern technological basis.”

China is not seen to play an active role in Patrushev’s remarks, but the geopolitical route is clear: “Russia is moving from the European market to the African, Asian and Latin American markets.” Russia would strengthen its cooperation with the other BRICS countries, i.e., Brazil, India, China and South Africa, and the Shanghai Cooperation Organization (SCO), where India and Pakistan as well as four other countries are involved in addition to China and Russia. The Eurasian Economic Union would receive the most attention, Patrushev says. This is also the vehicle that Sergey Glazyev sees at the heart of the new system.

Source: Russiabriefing.com

A pact against the West

Alongside Russia, China is always looking for ways to circumvent the US dollar. In doing so, the two countries have been making common cause for years. This trend has intensified tremendously in 2022. The relationship between Moscow and Beijing seems to have never been better. The common enemy: the Western monetary system. As early as February, Russia announced that it would no longer use the US currency for exports to China at all.

In the run-up to the Beijing Olympics, Russia and China also concluded a new, huge gas deal. The euro was chosen as the settlement currency. A clear signal to the EU: Russia and China want to drop the US dollar, but would have no problem with the euro. However, this deal came about before the war and the sanctions against the Russians’ euro reserves.

And that’s not all. In early February, shortly before Putin’s invasion of Ukraine, Russia and China concluded their largest friendship treaty ever. It is not a formal alliance – for such are fundamentally rejected by China – but it is a pact against America and the West. It is a document that historians might regard as the beginning of a new Cold War, a view also held in the West. Thus writes the New Yorker:

“Agreements between Moscow and Beijing, including the Treaty of Friendship of 2001, have traditionally been laden with lofty, if vague, rhetoric that faded into forgotten history. But the new and detailed five-thousand-word agreement is more than a collection of the usual tropes, Robert Daly, the director of the Kissinger Institute on China and the United States, at the Wilson Center, in Washington, told me. Although it falls short of a formal alliance, like NATO, the agreement reflects a more elaborate show of solidarity than any time in the past. ‘This is a pledge to stand shoulder to shoulder against America and the West, ideologically as well as militarily,’ Daly said. ‘This statement might be looked back on as the beginning of Cold War Two.’”

It has been 14 years since the financial crisis triggered by the US real estate market. Even then, in 2008, when Beijing hosted the Summer Olympic Games, Putin arrived as a guest with a hefty proposal, as then-US Treasury Secretary Hank Paulson describes in his book:

“Putin’s proposal was that Russia and China attack the US economically by selling massive amounts of US bonds issued by mortgage lenders Fannie Mae and Freddie Mac, to trigger a huge financial crisis and bring the common enemy to its knees.”

China refused at the time, but the Ukraine war and the new pact between Russia and China have changed everything. The friendship between the Russians and Chinese has certainly never been as solid as it is today. Putin and Xi refer to the relationship as a “partnership without limits.” In other words, no area of foreign security or economic policy is left out. The Europeans had to experience what this means at a virtual summit with China in early April. Again, Xi backed his ally Putin by deciding to do nothing. Officially, this was a big disappointment for the Europeans, who had hoped that Beijing would put pressure on Moscow.

EU representatives under Josep Borrell had hoped that Xi would take advantage of his good relationship with Putin to get him to negotiate peace with Ukraine. Nothing of the sort happened. China did nothing at all, signaling support for Russia in the Ukraine crisis. Borrell later called the EU-China parley a “dialogue of the deaf.” A month later, Beijing is clearly showing where its loyalties lie, even calling the friendship pact with Russia a “new model of international relations.”

Because, like Russia, China has much to gain in a world that is no longer dominated by the dollar. That’s why Beijing is also lobbying heavily in Saudi Arabia, the US’s most important ally in the Middle East; and China’s chances have never been better.

Xi and MBS – Pretty Much Best Friends

Only a few weeks after the Russian invasion of Ukraine, an invitation was sent from Riyadh to Beijing: President Xi Jinping should pay a visit to the kingdom. It was the clearest signal yet from Saudi Arabia that the oil state is turning eastward. The relationship with their traditional ally, the United States, has been in tatters for some time. This is most evident at the personal level. Crown Prince Mohammed bin Salman (MBS) had gotten along well with former President Donald Trump. Trump flew to Riyadh on his very first trip abroad and was received with much fanfare. It’s an honor the Saudis now want to bestow on the Chinese president.

The Wall Street Journal quotes a Saudi official: “The crown prince and Xi are close friends and both understand that there is huge potential for stronger ties. It is not just ‘They buy oil from us and we buy weapons from them.’”

The young crown prince is not on friendly terms with US President Joe Biden. Virtually every article about the rapprochement between the Saudis and the Chinese mentions how difficult the relationship between Riyadh and Washington is. Biden was vice president under Barack Obama, who actively turned his back on Saudi Arabia and struck the Iran nuclear deal. That deal was important to China, Russia and Europe – and was later rescinded by Trump.

Biden holds MBS responsible for the murder of journalist Jamal Khashoggi. He also refuses to treat MBS as a political equal to the US president. The official head of state remains King Faisal, MBS’s father. In a long interview with US magazine The Atlantic, MBS makes it clear where this American strategy is driving him: eastward, toward the Chinese: “Where is the potential in the world today? It’s in Saudi Arabia. And if you want to miss it, I believe other people in the East are going to be super happy.”

After the start of the war in Ukraine, the White House may have suddenly changed its position. Thus, the Wall Street Journal reported an attempt to contact MBS. But the crown prince refused to take a call from Joe Biden. And Sheikh Mohammed bin Zayed, the ruler of the United Arab Emirates, also declined to talk to Biden.

The Gulf states are indignant about the lack of support for Saudi Arabia’s war in Yemen and the resumption of negotiations with Iran under Biden. The rulers of the oil states, however, had no qualms about holding telephone conversations with Russian President Vladimir Putin. The tensions between Washington and the Arab world cannot be illustrated much more clearly.

There are no such tensions with China. MBS and Xi are “good friends”. Saudi Arabia is also a central pillar of China’s Belt and Road Initiative and in the top three when it comes to Chinese construction projects abroad. Here, the Chinese renminbi is also already involved as a currency.

All of this is important. After all, Saudi Arabia has always been the US’s central ally in the Middle East and was the decisive factor in establishing the petrodollar system. However, China has long been the oil state’s largest customer. To date, about 80 percent of the global oil market has been transacted in US dollars, and Saudi Arabia has probably been the decisive factor – for decades. But Beijing wants to finally switch the oil trade to the renminbi.

Some 25 percent of Saudi oil exports already go to China, and never have we been closer to a switch to renminbi than in 2022. Russia’s attack, sanctions, and Moscow’s response have shaken up international trade in energy and currencies. Ahead of Xi’s possible visit in May, Saudi Arabia again signaled a willingness to accept yuan (renminbi) soon.

Negotiations in this regard have been ongoing since 2016. In 2019, Saudi Aramco, the state oil company, presented plans for bonds in renminbi. China is also actively pursuing better relations with Saudi Arabia. It supports Riyadh in a nuclear program and has invested in the crown prince’s favorite project, the futuristic city of Neom.

In February 2022, plans were revived to jointly build an oil refinery in China. This project has been in planning since 2019, but it was put on hold during the pandemic because of low oil prices. Now it is topical again:

“The fact that this landmark refinery joint venture is back under serious consideration underlines the extremely significant shift in Saudi Arabia’s geopolitical alliances in the past few years – principally away from the US and its allies and toward China and its allies.”

The fact that Norinco, one of the two Chinese companies in this joint venture, is also one of China’s largest arms manufacturers should not go unmentioned; nor should Saudi Arabia’s plans to buy Russian missile systems.

The deal between Riyadh and Washington always had a military component. Protection and material were to be supplied by the US in exchange for oil – and the pricing of oil – in US dollars. But Saudi Arabia is not only diversifying in the oil trade. Since late 2021, it has also been working with China on a missile program. It seems that the exclusive relations between Saudi Arabia and the US are finally history.

It is only a matter of time before an extremely important oil nation, like Russia, accepts currencies other than the US dollar: renminbi, rupees, or maybe even euros. Russia, along with Saudi Arabia, Angola and Iraq, is one of China’s most important oil suppliers and will be ready at any time to sell even more oil in exchange for renminbi. According to our friends at Gavekal, this increases the pressure on Riyadh, because Beijing can use the oil trade with Russia as a good argument:

“China is the world’s largest oil importer, so what happens if Beijing tells Saudi and other Middle Eastern producers ‘I would love to do more business with you. But when I trade with Russia, that business is denominated in renminbi. Which works so much better for me. So unless you can take renminbi as well, I will likely import more energy from Russia.”

The consequences of these developments for the US dollar and thus for the international monetary and financial system are serious.

Gal Luft, co-director of the Institute for the Analysis of Global Security in Washington, says: “The oil market, and by extension the entire global commodities market, is the insurance policy of the status of the dollar as reserve currency. If that block is taken out of the wall, the wall will begin to collapse”.

Now, of course, there is more to consider in the question of whether the oil trade could be conducted in renminbi (yuan). China’s currency and economy are still hampered by strong capital controls. However, with many Chinese companies now operating in Saudi Arabia, the kingdom needs liquidity in Chinese currency. China is also very likely to promise further billions in investment in return for a currency conversion in the oil trade, which would further strengthen the link between the two states.

Conclusion: A New International Order Is Emerging

The sanctions against Russia, the response from Moscow, the Russians and Chinese moving closer together, the indecision of the Europeans, the new love between Saudi Arabia and China – that the world is in upheaval is obvious. Even the IMF, guardian of the US dollar order, is becoming active again. Kristalina Georgieva, managing director of the IMF, caused a stir with a statement in April:

“I think we are not paying sufficient attention to the law of unintended consequences. We take decisions with an objective in mind and rarely think through what may happen that is not our objective. And then we wrestle with the impact of it. Take any decision that is a massive decision, like the decision that we need to spend to support the economy. At that time, we did recognize that maybe too much money in circulation and too few goods, but didn’t really quite think through the consequence in a way that upfront would have informed better what we do.”

Then there was this big report that the IMF published shortly after the start of the Ukraine war. It bears the significant title “The Stealth Erosion of Dollar Dominance”. The report has a lot going for it, not least because the well-known economist Barry Eichengreen is a co-author.

Allocated Foreign Exchange Reserves not Held in USD, EUR, JPY and GBP, in % of World Total, Q1/1999-Q4/2021

Source: IMF, Incrementum AG

We find the choice of time period in the above chart particularly relevant. Around the turn of the millennium, the euro was established, the price of gold began to rise, and the dot-com bubble burst. Historically, this was arguably the turning point for the US dollar-dominated system. In our timeline, we show that things moved very quickly from that point on – and that the financial crisis, the pandemic and, most recently, the war in Ukraine accelerated the process further.

Hardly anything illustrates this development more impressively than this news item from the end of April 2022: Israel is cutting back on its US dollar and euro reserves and is investing reserves in yuan for the first time.

The freezing of Russia’s foreign exchange reserves was another nail in the coffin of the US dollar system. We do not know what exactly will take its place, but the trends we have documented in this chapter point in two directions: The world will become multipolar or bipolar, depending on Europe’s choices. And metals and commodities will become more important and either directly or indirectly involved in the monetary system.

We are at the end of a development that began in 1944. If Keynes had been listened to back then, perhaps the world would look different today. But the attempts to create a rules-based monetary system have all failed. Politicians like to tout Special Drawing Rights as an option, but that could just be a distraction, a way to point out dissatisfaction with the US dollar system without immediately bringing their own solution into play. The euro is perhaps the best example of what occurs with a rules-based international monetary system: The rules were immediately broken. But the euro’s strong gold component should also equip it for the other path, the one that China and Russia are already signaling very clearly: a world in which currencies find their anchor in reality – through reference to commodities, without a direct peg, but designed as a flexible system that is tested daily by the market.

It is not easy to put this new monetary order into words, as it is extremely dynamic. But the statements and actions of state leaders, as well as analyses such as those by Zoltan Pozsar and Luke Gromen, all point in this direction. Let’s not forget that the US has large reserves of raw materials – and 8,000 tonnes of gold. These have been lying around unused since Richard Nixon declared the gold window closed.

Now, it opens again.

[1] See “A Brief History of Gold Confiscations,” In Gold We Trust report 2021

[2] Moffitt, Michael: World’s Money, 1983, p. 196